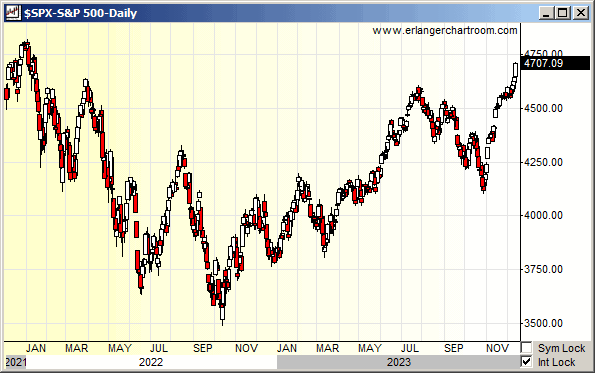

QPI Note - 12/14/23: S&P 500 Back Above 4700 For The First Time Since January of 2022.

Overnight Summary: The S&P 500 closed Wednesday higher by 1.37% at 4707.09 from Tuesday higher by 0.46% at 4643.70. The overnight high was hit at 4781.25 at 9:35 p.m. EST while the low was hit at 4758.25 at 5:00 p.m. EST. The range overnight was 23 points as of 6:25 a.m. EST. The 10-day average of the overnight range is at 15.70 from 14.60. The average for May-November average was 21.43 from 22.06. Currently, the S&P 500 is higher by 11.75 at 6:10 a.m. EST.

Executive Summary: Well, markets took Federal Reserve Chairman's dovish stance hook, line and sinker bidding stocks higher as we saw yields break 4.00% on the 10 year which is a first since the close of July. It was also the first close above 4700 since the first week of January in 2022. As Jerry Garcia said, "What a long strange trip its been." Two data economic data points out this morning of note that confirm or deny the action of yesterday.

Jobless Claims 8:30 a.m. EST

November Retail Sales are due out at 8:30 a.m. EST and are expected to stay at -0.1%.

Unusual Options Activity:

Daily Screen in Erlanger Chartroom that highlights unusual Call and Put Options activity in the S&P 500. It looks for volume outliers relative to the Open interest in Calls or puts. Usually, the stock price activity reflects the outlier situation (earnings/buyout/announcement), but once in a while, you can uncover stocks prior to a pop or drop.

Earnings Out After The Close:

Beats: ADBE +0.14, NDSN +0.06, MWA +0.02 of note.

Capital Raises:

New SPACs launched/News:

Digital World Acquisition Corp (DWAC) received termination notices from PIPE Investors representing approximately $17,500,000 of the PIPE.

Secondaries Priced:

ASLE: Announces prices secondary offering of 4.0 mln shares of common stock by selling shareholders.

OCUL: Prices offering of 30.8 million shares of common stock at $3.25 per share.

Common Stock filings/Notes:

AXDX: Filed Form S-1.. Offering of Units.

BTTX: Filed Form S-1.. Up to 20,000,000 Shares of Common Stock.

MLSS: Announces Closing of $3.0 Million Public Offering of Common Stock.

OCUL: Commences public offering of its common stock; subsequent 15% share buyback. (Jefferies, BAC and Piper bookmanager)

SVRE: Filed Form f-1.. Up to 20,000,000 American Depositary Shares Representing 100,000,000 Ordinary Shares.

VERU: Proposed Public Offering of Common Stock. (RJ and Oppenheimer bookmanager)

Direct Offering:

AZ: Announces US$1.5 Million Registered Direct Offering of Common Shares and Common Warrants.

Selling Shareholders of note:

ASLE: Secondary Offering of Common Stock by selling shareholders. 4 Million shares. (RBC Underwriter)

NEXT: Filed Form S-3.. 44,900,323 shares of Common Stock for Sale by the Selling Stockholder.

Mixed Shelf Offerings:

PBA: Form F-10 Filed Mixed Shelf.

Capital Raise Summary From The TradeXchange, bringing traders and investors real time news and Squawk Box, and other sources.

News After The Close :

After Hours Movers:

NXU: +26% Nxu Engages in Strategic Partnership and Investment in Lynx Motors

TEX: +2.5% Insider Purchase

ADBE: -5.5% Earnings

PBA: -4% Announces Accretive Consolidation of Alliance Pipeline and Aux Sable, and Concurrent $1.1 Billion Bought Deal Offering of Subscription Receipts

News Items After the Close:

DJIA closes at all time highs.

Adobe (ADBE) shares slide on weaker-than-expected forecast for 2024. (CNBC)

JPMORGAN: “.. with the Committee signaling that further inflation progress will be sufficient for easier policy, we now look for a first cut in June (previously July) and for a target range 125bp lower by year end.” (Carl Q Cnbc)

Barclays Expects Fed To Deliver Three 25Bps Rate Cuts In 2024 Starting In June - Vs One December 2024 Rate Cut Expected Previously.

Goldman Sachs Now Sees Fed To Deliver Three Consecutive 25Bps Rate Cuts In March, May And June

DoubleLine’s Jeffrey Gundlach says 10-year Treasury yield will fall to 3% next year. (CNBC)

UBS Steps Up Bid to Claw Back Cash From Credit Suisse Defectors. (Bloomberg)

Alibaba (BABA) pumps $630 million more into Lazada in race with TikTok, Sea (NikkeiAsia)

Robinhood Markets (HOOD) crypto notional trading volumes up 74% at $4 billion for November 2023.

GM fires 9 execs at Cruise, may face $1.5 million in fines.

Exchange/Listing/Company Reorg and Personnel News:

3D Systems (DDD) appoints Jeffrey Creech as CFO.

Crown Castle (CCI) informed its employees that the Company has canceled the plan announced on October 18, 2023 to relocate approximately 1,000 employee positions to a centralized location.

EOG Resources (EOG) promotes Jeffrey R. Leitzell to COO, promotes Ann D. Janssen to CFO.

KKR announces the appointment of Dane Holmes as Chief Administrative Officer.

Light & Wonder (LNW) appoints Oliver Chow as Executive Vice President, CFO, and Treasurer.

MAA Appoints Brad Hill to President and Chief Investment Officer.

Marten Transport (MRTN) appoints Adam D. Phillips to COO.

Mercury General (MCY) promotes Victor Joseph to COO position.

Quanex (NX) announces that George Wilson, the company’s President and Chief Executive Officer, will also become its Chairman of the Board.

RGS: NYSE Announces Intent to Commence Delisting Proceedings for Regis Corporation Common Stock; Opportunity to Appeal.

Veradigm Inc. (MDRX) Announces that Nasdaq Hearings Panel has Granted its Continued Listing, Pending Return to Compliance with Nasdaq Filing Requirements.

Buyback Announcements or News:

Cadence Bank (CADE) announces 2024 share repurchase program to purchase up to an aggregate of 10 million common stocks.

New Mountain Finance Corporation (NMFC) Announces the Extension of its Stock Repurchase Program. (see Dividends below)

Seadrill (SDRL) initiates new $250 million share reppurchase program .

Toll Brothers (TOL) approves new 20 million share repurchase authorization replacing its current program. (see Dividends below)

Stock Splits or News:

Virax Biolabs Group Limited (VRAX) Announces 1-for-10 Share Consolidation.

Dividends Announcements or News:

American Eagle (AEO) raises its quarterly dividend by 25% to $0.125 per share; 2.4% annual yield.

ARMOUR Residential REIT (ARR) reduces monthly dividend to $0.24 per share for January, down from $0.40 pre share prior

New Mountain Finance Corporation (NMFC) Declares a Special Distribution.

Preferred Bank (PFBC) increases its quarterly dividend 27.3% to $0.70 per share; 4.0% annual yield.

SITE Centers (SITC) declares cash special dividend of $0.16 per share.

Toll Brothers (TOL) announces dividend.

Insider Sales Of Note: None of note.

What’s Happening This Morning: Futures value reflects the change with fair value.

S&P 500 +15, Dow Jones +129, NASDAQ +66, and Russell 2000 +28. (as of 7:58 a.m. EST). Asia is higher ex the Nikkei while Europe is higher this morning. VIX Futures are at 14.05 from 14.35 this morning. Gold, Silver and Copper are higher this morning. WTI Crude Oil and Brent Crude Oil are higher with Natural Gas higher as well. US 10-year Treasury sees yields at 3.947% from 4.18% yesterday. The U.S. Dollar is lower versus the Euro, lower versus the Pound and lower against the Yen. Bitcoin is at $43,000 from $41,108 higher by +0.51% this morning.

Sector Action:

Daily Positive Sectors: Utilities, Real Estate, Basic Materials, Healthcare, Financial, Consumer Defensive of note.

Daily Negative Sectors: Definitely none of note.

Investors searched for hints Wednesday on whether the Federal Reserve might begin cutting interest rates next year. The central bank didn’t disappoint. Stocks hovered near the flatline throughout the trading session until Fed members unanimously voted to hold rates steady and signaled that they could begin easing monetary policy next year. While Chair Jerome Powell left the possibility of additional hikes on the table, markets paid little attention. The S&P 500 and tech-heavy Nasdaq Composite rose 1.4% apiece. The Dow Jones Industrial Average breached 37000 for the first time, settling at an all-time high of 37090. (WSJ - edited by QPI)

Upcoming Earnings Of Note: (From Chartroom Software - sorted by market cap, highest to lowest with most visible names)

Thursday After the Close:

Friday Before the Open:

Earnings of Note This Morning:

Still to Report: JBL of note.

Company Earnings Guidance:

Positive Guidance: DESP, GKOS of note.

Negative Guidance: MWA, NDSN, NUE of note.

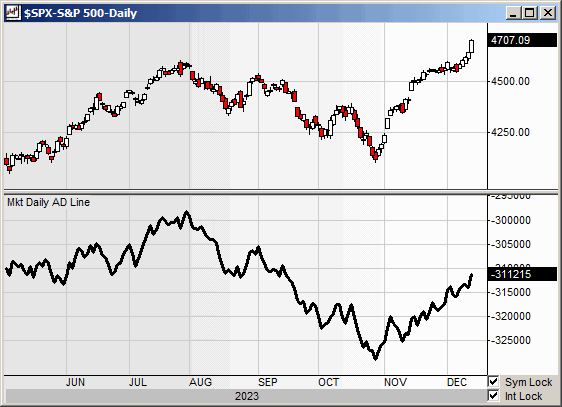

Erlanger Research Advance/Decline Chart:

Gap Ups & Down In Early Pre-Market:

Gap Up: ESPR +14%, CDXS +13%, SDRL +6% of note.

Gap Down: OCUL -17%, ASLE -10%, MDRX -10%, ADBE -5% of note.

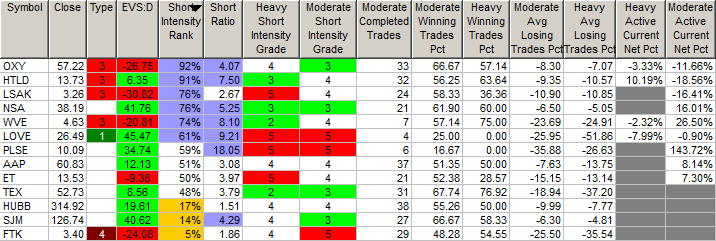

Insider Action: OXY, HTLD, NSA, WVE, AAP sees Insider buying with dumb short selling. LOVE, PLSE sees Insider buying with smart short sellers.

Rags & Mags.: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

Stocks making the biggest moves before the bell: MRNA, ADBE, LYV, UAL, DAL, FL, DHR, LEN, TRIP, OXY, OPEN (CNBC)

What You Need To Know To Start Your Day. (Bloomberg)

5 Things To Know Before the Stock Market Opens on Thursday. (CNBC)

Bloomberg Lead Story: Wall Street Traders Go All In On The Great Monetary Pivot 0f 2024 (Bloomberg)

Bloomberg Most Shared Story: Citigroup (C) offers early bonuses to encourage early departures. (Bloomberg)

Bank of England (BOE) leaves rates unchanged but warns of "higher for longer". (CNBC)

Here's why bringing down inflation is different this time says Chairman Powell. (CNBC)

IEA Survey shows oil demand dropping indicating a sharper slowdown. (Bloomberg)

BNP Strategist saws to overweight Europe over the U.S. (CNBC)

Merck (MRK) -Moderna (MRNA) vaccine cuts risk skin cancer returns by half. (Bloomberg)

Bloomberg The Big Take: The Presidential Race no one wants. (Podcast)

NPR Marketplace: Meta has a problem with hosting predators on its platform. (Podcast)

NY Times Daily: The woman who fought the Texas abortion ban. (Podcast)

Wealthion: Navigating the Global Energy Crisis with Daniel Yergin. (Podcast)

Moving Average Update:

100%. Day 4. Strong.

Geopolitical:

President’s Public Schedule:

The President receives the Presidential Daily Briefing, 10:00 a.m. EST

Press Briefing by Press Secretary Karine Jean-Pierre and NSC Coordinator for Strategic Communications John Kirby, 1:00 p.m. EST

The President departs the White House, 2:35 p.m. EST

The President delivers remarks on his administration’s progress to lower prescription drug costs, 3:15 p.m. EST

The President arrives at the White House, 4:30 p.m. EST

Economic:

Jobless Claims 8:30 a.m. EST

November Retail Sales are due out at 8:30 a.m. EST and are expected to stay at -0.1%.

Import and Export Prices 8:30 a.m. EST

Business Inventories 10:00 a.m. EST

Federal Reserve / Treasury Speakers: None of note.

M&A Activity and News:

Carrier Global (CARR) Announces agreement to sell carrier commercial refrigeration to Haier for $775 million, including approximately $200 million of net pension liabilities.

Certara (CERT) acquires Applied BioMath.

Pembina Pipeline (PBA) announces accretive acquisition of Enbridge’s (ENB) interests in Alliance for an aggregate purchase price of ~$3.1 billion.

Meeting & Conferences of Note:

Sellside Conferences:

Imperial Capital Security Investor Conference

Oppenheimer Midwest Summit

Stifel MedTech West Coast Bus Tour

Previously posted and ongoing conferences:

Bank of America STARS Summit

ROTH MKM Deer Valley Conference

Top Shareholder Meetings: AZPN, CTHR, FDS, FLWS, NTES, RIOT, WGO

Investor/Analyst Day/Calls: BCYC, CHWY, COHR, GOL, INTC, NVVE, PECO, REGN, REKR, SDGR, SPLK, WWR

Company Event:

Intel's (INTC) AI Everywhere Launch Event.

Industry Meetings:

IASLC Conference

Previously posted and ongoing conferences: None of note.

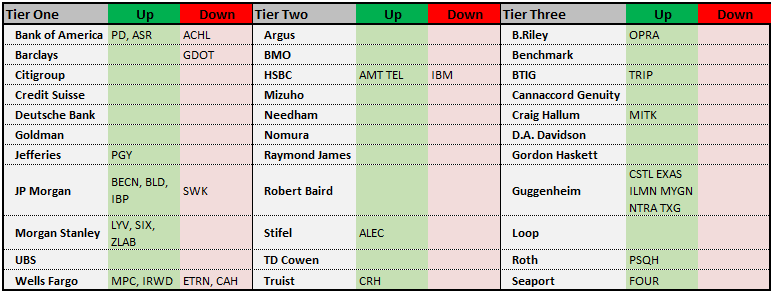

Top Tier Sell-side Upgrades & Downgrades: