QPI Note - 12/06/23: ADP Data Up Shortly, Stocks Up But Fade Overnight Highs

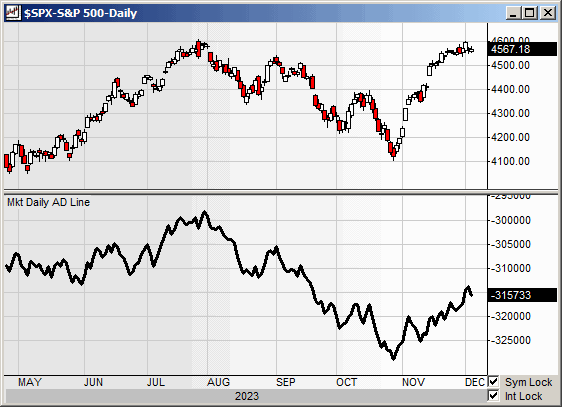

Overnight Summary: The S&P 500 closed Tuesday lower by -0.06% at 4567.18 from Monday lower by -0.54% at 4569.78. The overnight high was hit at 4590.25 at 10:50 p.m. EST while the low was hit at 4571.25 at 6:05 p.m. EST. The range overnight was 19 points as of 7:15 a.m. EST. The 10-day average of the overnight range is at 16.40 from 15.70. The average for May-October average was 22.06 from 20.96. Currently, the S&P 500 is higher by 7 points which is +0.15% at 7:20 a.m. EST.

Executive Summary: Putin made a visit to the Gulf in a rare trip out of Russia. We get the start of the job's data this morning with ADP Payroll. Watch the reaction by bonds as rates drop to new lows. Stocks are hanging tough but going sideways the last few days. Will it hold?

November ADP Employment Report is due out at 8:15 a.m. EST and expected to rise to 127,000 from 113,000.

Bank CEOs to testify on regulatory oversight. (Bloomberg)

Unusual Options Activity:

Daily Screen in Erlanger Chartroom that highlights unusual Call and Put Options activity in the S&P 500. It looks for volume outliers relative to the Open interest in Calls or puts. Usually, the stock price activity reflects the outlier situation (earnings/buyout/announcement), but once in a while, you can uncover stocks prior to a pop or drop.

Earnings Out After The Close:

Beats: MDB +0.45, TOL +0.39, AVAV +0.35, PLAY +0.16, PHR +0.10, ASAN +0.07, S +0.05, YEXT +0.02 of note.

Flat: None of note.

Misses: SFIX (0.05), BOX (0.02) of note.

Capital Raises:

New SPACs launched/News:

Eco Modular, a Leader in Sustainable Modular Building Manufacturing, to Go Public Through Merger with Zalatoris II Acquisition Corp (ZLS).

Secondaries Priced:

ATAT: Prices secondary offering of 9.6 million shares of common stock at $15.80 per share.

CRDO: Prices offering of 10.0 million shares of common stock at $17.50 per share.

EYPT: Prices offering of 11,764,706 shares of its common stock at $17.00 per share.

IPA: Announces Pricing of $1.1 Million Public Offering of Common Shares.

PHVS: Pricing of $300 Million Underwritten Offering of Ordinary Shares and Pre-funded Warrants.

SN: Prices secondary offering of 6,095,169 ordinary shares at $47.00 per ordinary share.

Notes Priced of note:

CACC: Announces Pricing of $600.0 Million Senior Notes Offering.

CRGY: Pricing of $150 Million Private Placement of Additional 9.250% Senior Notes Due 2028.

EVH: Prices offering of $350.0 million of convertible senior notes due 2029.

SPHR: Announces pricing of $225 million offering of convertible senior notes.

Common Stock filings/Notes:

CRDO: Launch of public offering.. 10,000,000 of its ordinary shares. (GS Bookmanager) (see Mixed Shelf and Pricing too)

FLNC: Announces Secondary Offering of Class A Common Stock by Existing Controlling Stockholders.

IPA: Proposed Public Offering of Common Shares.

POLA: Announces Closing of Public Offering.

SDIG: Filed Form S-3.. 2,798,590 Shares.

VTMX: Announces Proposed Follow-On Offering.

Direct Offering:

KZIA: Announces Closing of $2 Million Registered Direct Offering.

Private Placement of Public Entity (PIPE):

COYA: Announces $26.5 Million Private Placement.

Mixed Shelf Offerings:

CRDO: Filed Form S-3ASR.. $300,000,000 Mixed Shelf.

RY: Filed Form F-3.. Mixed Shelf Offering.

SKT: Filed Form S-3ASR .. Mixed Shelf.

SIG: Files mixed shelf securities offering.VRAX: Filed Form F-3.. $30 Million Mixed Security Shelf.

Debt/Credit Filing and Notes:

GBNH: Raises Us$2.5 Million In Debt Financing.

PFSI: Announces Proposed Private Offering of $650 Million of Senior Notes.

Convertible Offering & Notes Filed:

TREE: Repurchases portion of 2025 convertible notes.

Capital Raise Summary From The TradeXchange, bringing traders and investors real time news and Squawk Box, and other sources.

News After The Close :

After Hours Movers:

GBNH: +37% Raises $2.5 million in Debt Financing.

S: +21% Earnings

ACRS: +17% Patent License Agreement with Sun Pharma for Alopecia

PHR: +11% Earnings

TOL: +2.5% Earnings

YEXT: -11.5% Earnings

BOX: -11% Earnings

ASAN: -10% Earnings

FLNC: -9% Secondary Offering of Class A Common Stock by Existing Controlling Stockholders

MDB: -6% Earnings

CRDO: -5% launch of public offering

FIVN: -5% Responds to Market Rumor

PLAY: -3% Earnings

News Items After the Close:

Stocks making the biggest moves after hours: BOX, MDB, ASAN, NBIX, PLAY, TOL (CNBC)

Box’s (BOX) stock drops 11% on tepid revenue forecast. (MarketWatch)

MongoDB (MDB) earnings clear Wall Street’s bar, but stock falls. (MarketWatch)

Asana’s (ASAN) stock is falling after another quarterly loss. (MarketWatch)

Signet Jewelers (SIG) CEO says ‘engagement trough’ has passed. (CNBC)

Elon Musk’s AI startup — X.AI — files to raise $1 billion in fresh capital. (CNBC)

Exchange/Listing/Company Reorg and Personnel News:

Altisource Asset Management Corporation (AAMC) Announces Departure of COO and Interim CEO Danya Sawyer.

Aurora Mobile (JG) Announces Change to American Depositary Share Ratio.

AxoGen (AXGN) announces the appointment of Mr. Nir Naor as Chief Financial Officer.

GEO: Form 8K.. The GEO Group, Inc. (“GEO” or the “Company”) announced on November 30, 2023 that following discussions between GEO and its Chief Executive Officer, Jose Gordo, the parties agreed that Mr. Gordo will be departing as Chief Executive Officer and as a Board member on mutually agreeable terms and transitioning to the role of an advisor, effective December 31, 2023.

Lixiang Education (LXEH) Receives Nasdaq Extension to Regain $1 Bid Price Compliance.

MongoDB (MDB) Appoints Ann Lewnes to Board of Directors.

Powerbridge Technologies Co., Ltd. (PBTS) Announces Receipt of Nasdaq Notification Letter Regarding Minimum Bid Price Deficiency.

TIAN RUIXIANG Holdings Ltd (TIRX) Receives Nasdaq Notice of Deficiency Regarding Minimum Bid Price Requirement.

Buyback Announcements or News:

Butterfield (NTB) Announces Share Repurchase Program of $90 million ordinary shares.

Exxon (XOM) Increasing Pace Of Share-repurchase Program To $20b per year.

First Financial (FFBC) authorizes purchase of up to 5.0 mln shares of its common stock, representing approximately 5% of its outstanding shares of common stock.

Mastercard (MA) Board of Directors Announces $11 Billion Share Repurchase Program. (see Dividends)

Midland States Bancorp, Inc. (MSBI) Announces Authorization of New $25 Million Stock Repurchase Program.

OLP: Increases Current Share Repurchase Authorization.

Radiant Logistics (RLGT) Announces Renewal Of Its Stock Repurchase Program.

Sterling (STRL) Announces Authorization of a $200 Million Stock Repurchase Program.

Trustmark (TRMK) authorizes new stock repurchase program up to $50 million.

Stock Splits or News:

Cenntro Electric Group (CENN) Announces December 8, 2023 Effective Date for Reverse Stock Split to Regain Nasdaq Compliance.

Instil Bio (TIL) Announces Effective Date of 1-for-20 Reverse Stock Split.

Dividends Announcements or News:

Avis Budget Group (CAR) Announces Special Cash Dividend.

Balchem (BCPC) raises its annual dividend by 11% to $0.79 per share; annual yield of 0.6%.

Coca-Cola Consolidated (COKE) declares a special dividend of $16.00 per share.

Danaher (DHR) decreases quarterly cash dividend to $0.24 per share from $0.27 per share

Hooker Furnishings (HOFT) Declares Increased Quarterly Dividend.

Mastercard (MA) increases quarterly cash dividend to $0.66 per share from $0.57 per share.

Quanta Services (PWR) increases quarterly dividend 12.5% to $0.36 per share.

PNM Resources (PNM) increases quarterly cash dividend 5.4% to $0.3875 per share from $0.3675 per share.

Upbound Group (UPBD) increases quarterly cash dividend ~9% to $0.37 per share from $0.34 per share.

Insider Sales Of Note: None of note.

What’s Happening This Morning: Futures value reflects the change with fair value.

S&P 500 +10, Dow Jones +60, NASDAQ +41, and Russell 2000 +6. (as of 7:59 a.m. EST). Asia and Europe are higher this morning. VIX Futures are at 13.60 from 13.90 this morning. Gold is higher with Silver lower and Copper higher this morning. WTI Crude Oil and Brent Crude Oil are lower with Natural Gas higher. US 10-year Treasury sees yields at 4.193% from 4.243% yesterday. The U.S. Dollar is higher versus the Euro, higher versus the Pound and higher against the Yen. Bitcoin is at $43,956 from $41,697 higher by +0.61% this morning.

Sector Action:

Daily Positive Sectors: Technology of note.

Daily Negative Sectors: Energy, Basic Materials, Industrials, Utilities, Real Estate, Consumer Defensive, Financial of note.

The bond rally resumed Tuesday, driving yields on benchmark 10-year U.S. notes to their lowest level since summer and lifting technology shares on an otherwise downbeat day for stocks. The technology-heavy Nasdaq Composite added 0.3%. In the S&P 500, technology and consumer-discretionary shares failed to offset declines in utilities, energy, materials and real-estate stocks, and the broad index shed less than 0.1%. The Dow Jones Industrial Average fell 0.2%, or about 80 points. The yield on the 10-year Treasury notes ended at 4.171%, down from 4.286% on Monday and well off the 5% hit in late October. The yield, which falls as prices rise, hasn’t been so low since Aug. 31. (WSJ - edited by QPI)

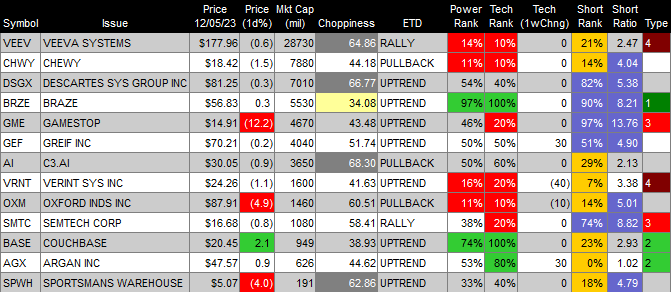

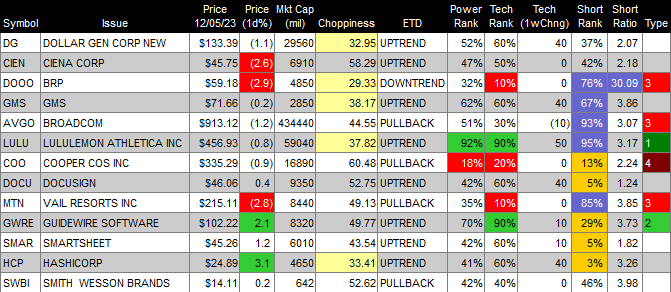

Upcoming Earnings Of Note: (From Chartroom Software - sorted by market cap, highest to lowest with most visible names)

Wednesday After the Close:

Thursday Before the Open:

Earnings of Note This Morning:

Beats: UNFI +0.28, LOVE +0.15, OLLI +0.06CPB +0.04, HO +0.03, KFY +0.02 of note.

Misses: BF.B (0.01) of note.

Company Earnings Guidance:

Positive Guidance: HQY, MDB, ASAN, S, OLLI of note.

Negative Guidance: PHR, BOX, YEXT, INMD of note.

Erlanger Research Advance/Decline Chart:

Gap Ups & Down In Early Pre-Market:

Gap Up: S +18%, PHR +14%, ASPN +14%, SFIX +8%, EYPT +7%, CAR +4%, ATAT +4% of note.

Gap Down: BOX -15%, YEXT -14%, ASAN -13%, FLNC -10%, OOMA -7%, BTI -7%, CRDO -5%, MDB -4% of note.

Insider Action: DINO, HHS, HTLD, SCVL sees Insider buying with dumb short selling. PLSE sees Insider buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

Stocks making the biggest moves premarket: SHOP, TOST, PYPL SPHR, DFS, ASAN, COF, BLDR (CNBC)

What You Need To Know To Start Your Day. (Bloomberg)

5 Things To Know Before the Stock Market Opens on Wednesday. (CNBC)

Bloomberg Lead Story: Putin visits the Gulf in rare foreign trip. (Bloomberg)

Bloomberg Second Most Shared Story: Biden says might not have run for reelection if Trump was not running. (Bloomberg)

Stocks keep rate-cut faith as bond rally falters: Market Wrap. (Bloomberg)

Russian President Putin visits the U.A.E. and Saudi Arabia in a rare visit. (CNBC)

Mortgage refinance demand pops 14% in latest week as rates continue to drop. (CNBC)

Robinhood (HOOD) CEO was interviewed this morning on CNBC. (CNBC)

Bumper travel year in 2024. (CNBC)

Bloomberg The Big Take: It's not a good time to buy a home, anywhere. (Podcast)

NPR Marketplace: Meta's pixel code tracks from kindergarten to college. (Podcast)

NY Times Daily: Will Supreme Court reject Opiod Settlement? (Podcast)

BBC Global News Daily Podcast: Fiercest day of fighting in Gaza. (Podcast)

Wealthion: Former White house Economist reveals recession warning signs. (Podcast)

Moving Average Update:

Down to 80% from 82%.

Geopolitical:

President’s Public Schedule:

The President receives the Presidential Daily Briefing, 9:00 p.m. EST

The President participates in a meeting with G7 leaders [Virtual], 9:30 a.m. EST

The President departs the White House en route the White House Tribal Nations Summit, 1:10 p.m. EST

The President delivers remarks at the White House Tribal Nations Summit, 1:45 p.m. EST

The President departs the White House Tribal Nations Summit en route to the White House, 2:30 p.m. EST

The President arrives at the White House, 2:35 p.m. EST

Press Briefing by Press Secretary Karine Jean-Pierre and NSC Coordinator for Strategic Communications John Kirby, 2:45 p.m. EST

The President departs the White House en route to the St. Regis Hotel, Washington, DC, 4:50 p.m. EST

The President participates in a campaign reception, 5:30 p.m. EST

The President arrives at the White House, 6:15 p.m. EST

Economic:

MBA Mortgage Applications 7:00 a.m. EST

November ADP Employment Report is due out at 8:15 a.m. EST and expected to rise to 127,000 from 113,000.

Int. Trade in Goods 8:30 a.m. EST

Productivity and Costs 8:30 a.m. EST

EIA Petroleum Report 10:30 a.m. EST

Federal Reserve / Treasury Speakers:

Fed Blackout Period.

M&A Activity and News:

R1 RCM (RCM) announced that it has entered into a definitive agreement to acquire Acclara.

Meeting & Conferences of Note:

Sellside Conferences:

Barclays Global Technology Conference

Deutsche Bank's Lithium Battery Supply Chain Conference

Jefferies Private MedTech Summit

Mizuho Medical Device and Healthcare Services Summit

Roth Sustainability Private Capital Event

Sidoti December Small Cap Conference

Wainwright Precision Oncology Virtual Conference

Wolfe Research Small and Mid-Cap Conference

Previously posted and ongoing conferences:

Credit Suisse Climate Tech Conference

Goldman Sachs Financial Services Conference

Janney Clean Energy Investment Symposium

JMP Securities Hematology and Oncology Summit

Morgan Stanley Global Consumer & Retail Conference

Raymond James TMT & Consumer Conference

Wells Fargo Midstream and Utility Symposium

Top Shareholder Meetings: ALTU, CSCO, FSI, MSGE, SGBX, TEAM

Investor/Analyst Day/Calls: ACRX, AMD, CEVA, ED, MCD, MNDY, OMF, OMI, SLGL, XOM

Industry Meetings:

United Nations Climate Change Conference

Emerging Growth Conference

Previously posted and ongoing conferences:

Nasdaq Investor Conference

San Antonio Breast Cancer Symposium

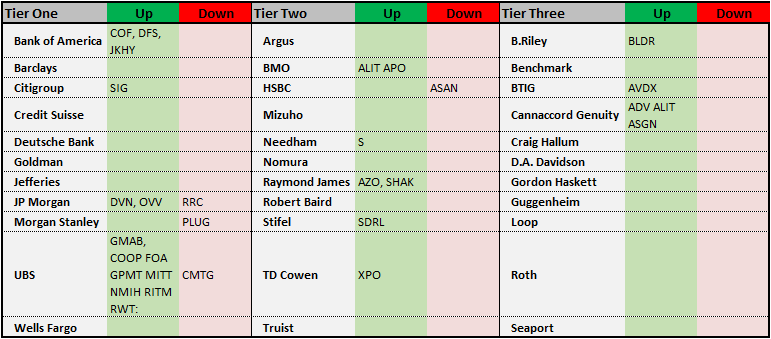

Top Tier Sell-side Upgrades & Downgrades: