QPI Morning Note - Political Posturing By DOJ and Candidates Hits Stocks This Morning

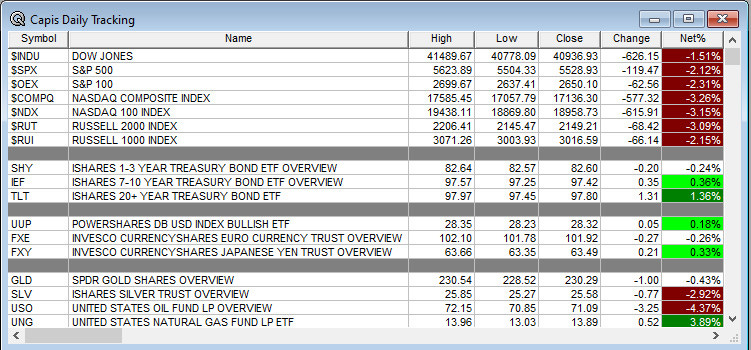

Overnight Summary: The S&P 500 closed Tuesday lower by -2.12% at 5528.93 from Friday higher by 1.01% at 5648.10. The overnight high was hit at 5,545.50 at 4:05 p.m. EDT and the low was hit at 5506.75 at 3:00 a.m. EDT. The overnight range is 39 points. The current price is 5522.25 at 7:00 a.m. EDT lower by -19.50 points.

Most Important Article Of the Morning: The Dumbest Idea of the Presidential Campaign – All Candidates oppose U.S. Steel (X) purchase by Nippon. (WSJ)

Executive Summary:

52 Week Bill Auction at 1:00 p.m. EDT.

Factory orders and JOLTS out at 10:00.

Fed Beige Book out at 2:00 p.m. EDT.

Earnings Out After The Close:

Beats: ZS +0.18, HQY +0.16, GTLB +0.05, PD +0.04, ASAN +0.03 of note.

Flat:

Misses: None of note.

Capital Raises:

IPOs For The Week: CUPR, GLXG, JBDI, PMAX, TDTH

New IPOs/SPACs launched/News:

IPOs Filed/Priced:

Secondaries Filed or Priced:

PCVX commences $1 bln stock offering and pre-funded warrants

IRT commences 10 mln share offering

STWD announces public offering of 17.4 mln common stock

PACS announces commencement of 13,888,890 share offering, consisting of 2,777,778 shares sold by the company

REVB: Form S-3.. 5,096,120 Shares of Common Stock

ULS – Launch of Proposed Secondary Public Offering of Class A Common Stock – 20,000,000

shares.XTNT: Form S-3.. 7,812,500 Shares of Common Stock

ZPTA: Form S-1.. Up to 13,000,000 Shares of Common Stock

ZVSA: Form S-3.. 478,600 Shares of Common Stock

Notes Priced:

AER Pricing of $2.4 Billion Aggregate Principal Amount of Senior Notes

MGM Prices $850,000,000 in Senior Notes

Direct Offering:

Exchangeable Subordinate Voting Shares:

Selling Shareholders of note:

PACS to sell 11,111,112 shares sold by certain selling stockholders

Debt/Credit Filing and Notes:

Mixed Shelf Offerings:

ZURA files $300 mln mixed shelf securities offering

CIFR files mixed shelf securities offering

AKBA: FORM S-3 – $250,000,000 Mixed Shelf Offering

PIPE:

Convertible Offering & Notes Filed:

Capital Raise Summary From The TradeXchange, bringing traders and investors real time news and Squawk Box, and other sources.

Biggest Movers Up & Down After The Close:

Movers Up: CLOV +20%, GTLB +12.4%, AURA +7.2%, CLLS +3.5%, RNG +2%.

Movers Down: ATHA -75%, ULS -4.8%, IRT -43.%, PACS -3.5%, STWD -3.1%, MGX -2.4%, NVDA -2.3%,

News After Thsee Close :

GO announces official launch of new private label program called Go Brands

ESI announces definitive agreement to sell MacDermid Graphics Solutions to XSYS for ~$325 mln.

RYAM announces that, effective immediately, it will increase prices for its Cellulose Specialties products by up to 10%, depending on product grade, as contracts allow

NVDA sliding by over -1.0% after receiving DOJ subpoena in escalating antitrust probe. (Bloomberg)

GPK now expects FY24 adjusted EPS below mid-point of prior guidance due to weather events

CP provides 2024 outlook and long-term growth forecasts in Investor Presentation; expects double-digit core adjusted EPS growth in FY24

EW completes sale of Critical Care product group to BD (BDX) for $4.2 bln.

NOC awarded $198 mln U.S. Navy contract

10-Q or 10-K Delays – None of note.

NASDAQ Delisting Notice – None of note.

Buybacks or Repurchases: Buybacks should be slow as most companies are in a blackout period as earnings season kicks into gear.

HQY authorizes $300 million in buybacks.

EW announces $1 billion share repurchase program

ATHM approves new $200 mln share repurchase program

Exchange/Listing/Company Reorg and Personnel News:

RNG announces that Sonalee Parekh has resigned as CFO, effective September 10; will start a search for new CFO.

ASAN names Sonalee Parekh, as its new CFO, effective September 11; to succeed Tim Wan, who will remain with the company in an advisory position

ARAY President and CEO to take a temporary medical leave of absence; Senior Vice President and Chief Commercial Officer, Sandeep Chalke, will serve as interim CEO

AMD announces that Keith Strier, who most recently served as vice president of worldwide AI initiatives at NVIDIA, will join company as senior vice president of global AI markets

Dividends Announcements or News:

Stocks Ex Div Today: CI SLB ODFY HKKCY HAL FOX FOXA AVY LUV TXRH ALV LEA PVH

Stocks Ex Div Tomorrow: QCOM NEM STE TER PFG KIM AEG MOS HRB CBSH JXN

PECO increases monthly dividend 5.1% to $0.1025/share

STC increases quarterly cash dividend to $0.50/share from $0.475/share

KLAC increases quarterly cash dividend 17% to $1.70/share from $1.45/share

What’s Happening This Morning: Futures S&P 500 -25 NASDAQ 100 -148 Dow Jones -91 Russell 2000 -11.41. Asia and Europe are lower this morning. VIX Futures are at 19.35 from 15.80 yesterday while Bonds are at 3.814% from 3.917% on the 10-Year. Crude Oil and Brent are higher with Natural Gas flat. Gold is lower with Silver higher and Copper lower. The U.S. Dollar is lower versus the Euro, higher versus the Pound and lower against the Yen. Bitcoin is at $56,645 from $59,067 lower by 2.32% this morning.

Sector Action – (1/3/6/12/YTD Updated Weekly with Monday release):

Daily Positive Sectors: Consumer Defensive of note.

Daily Negative Sectors: Technology, Materials, Industrials and Energy of note.

One Month Winners: Financials, Technology, Real Estate, Utilities, Consumer Defensive, Industrials and Healthcare of note.

Three Month Winners: Technology, Real Estate, Healthcare, Financials and

Utilitiesof note.Six Month Winners: Utilities, Technology, Communication Services, Financials, Real Estate and Consumer Defensive of note.

Twelve Month Winners: Technology, Communication Services, Financials, Industrials, Utilities, and Healthcare note.

Year to Date Winners: Technology, Communication Services, Utilities, Financials, Consumer Defensive and Healthcare of note.

Upcoming Earnings Of Note: (From Chartroom Software – sorted by market cap, highest to lowest with most visible names)

Wednesday After the Close: None of Note

Thursday Before The Open:

Earnings of Note This Morning:

Beats: DKS +0.51, CIEN +0.09, REVG +0,06, HRL +0.01, CURV +0.01, of note.

Flat:

Misses: CRMT -0.81, DLTR -0.37, CNM -0.13 of note.

Still to Report:

Company Earnings Guidance:

Positive Guidance: GTLB of note.

Negative or Mixed Guidance: ZS CNM of note.

Advance/Decline Weekly Update With Both Daily and Weekly Stats: Tuesday was ugly!!

Gap Ups & Down In Early Pre-Market (+2% or down more than -2%):

Gap Up: GTLB +16.9%, AURA +12.3%, CLOV +8.8%, GO +4.9%, MNOV +3.6%, CLLS +3.1%, HLX +3.1%, MGX +2.1%

Gap Down: ATHA -72.8%, ASND -19.1%, ZS -15.3%, PD -14.7%, ASAN -14.6%, OS -3.9%, STWD -3.2%, PACS -3.1%, ULS -2.1%, AKBA -2.1%

Insider Action: ESTC see Insider buying with dumb short selling. None of note see Insider buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

5 Things To Know Before The Stock Market Opens Today. (CNBC)

What You Need To Know to Start your Day. (Bloomberg)

Bloomberg Lead Story: Nvidia Has Traders Watching The $100 Level. (Bloomberg)

Markets Wrap: US Futures signal weaker open as Nvidia slips. (Bloomberg)

Pre-Market Movers . (CNBC)

Vice President Harris proposes $50k small business startup tax break. (CNBC)

Jim Cramer calls DELL a bargain at current level. (CNBC)

Bloomberg Big Take: Getting asylum in the US boils down to luck. (Podcast)

NYT Times Daily: The Battle To Control AI and Nvidia. (Podcast)

Marketplace: AI Safety Bill dividing Silicon Valley. (Podcast)

Wealthion: Recession is Here: Why Gold and Uranium are your best bets. (Podcast)

Economic:

July Factory Orders are due out at 10:00 a.m. EDT and expected to climb to 4.5% from -3.3%.

The latest JOLTS Survey is due out at 10:00 a.m. EDT.

Weekly MBA Mortgage Applications grew 1.6% from 0.5% a week ago.

The latest Federal Reserve Beige Book is due out at 2:00 p.m. EDT.

Weekly API Crude Oil Data is due out at 4:30 p.m. EDT.

Geopolitical:

President Biden receives the Daily Briefing at 11:00 a.m. EDT.

Press Briefing by Press Secretary Karine Jean-Pierre and Director of the Office of Intergovernmental Affairs Tom Perez.

Federal Reserve Speakers

None of note today.

M&A Activity and News:

None of note.

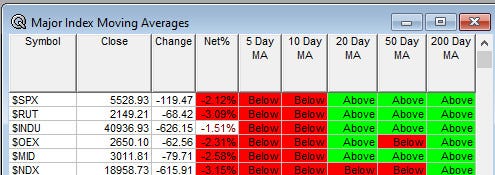

Moving Averages On Major Indexes: Moves from 97% to 50% of the moving averages being positive.

Meeting & Conferences of Note:

Sellside Conferences:

Bank of America Media Communications and Entertainment Conference

Barclays Global Consumer Staples Conference

Barclays CEO Energy Power Conference

Benchmark Tech Media & Telecom Conference

Citi Global Technology Conference

Deutsche Bank Aircraft Finance & Leasing Conference

Goldman Sachs Global Retailing Conference

J.P. Morgan European Healthcare CEO Call Series

Jefferies Industrials Conference

KBW Insurance Conference

Morgan Stanley Global HealthCare Conference

Raymond James 2024 U.S. Bank and Banking on Tech Conferences

Stifel London Industrial Conference

UBS Global Emerging Markets Conference

Wells Fargo Healthcare Conference

Fireside Chat: None of note.

Top Shareholder Meetings: BKSY, CDXS, CGNT, LOGI, REPL, UA

Investor/Analyst Day/Calls: BMRN, DHR, NVTS, RVPH

Update: None of note.

R&D Day: None of note.

FDA Presentation:

Company Event:

Industry Meetings or Events:

PAINWeek Conference 2024

SEMICON Taiwan 2024

Top Tier Sell-side Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from QPI or its employees.

Upgrades: NDAQ FCX ERJ

Downgrades: