QPI Morning Note For 05/06/25: Futures Weak A Second Day In A Row, Have Markets Lost That Loving Feeling?

Overnight Summary & Early Morning Trading:

The S&P 500 finished Monday lower by -0.64% at 5650.38. Friday higher by 1.47% at 5686.67. Futures are lower this morning by -39.50 (-0.70%) at 5632.25 around 6:00 a.m. EDT. The range is now 500 points on the S&P 500 cash for the year, 5600 to 6100. Year to date the S&P 500 is down -3.93% from -3.31% Thursday's close.

Executive Summary:

Stocks are beginning to trade with less volatility as the VIX is below 25. The S&P 500 broke its nine-day win streak on Monday.

Key Events of Note Today:

March Trade Balance is out at 8:30 a.m. EDT.

Weekly API Petroleum Data is due out at 4:30 p.m. EDT.

3 & 6-Month Bill Auction at 11:30 a.m. EDT

3-Year Note Auction at 1:00 p.m. EDT.

Notable Earnings Out After The Close:

Beats: LMB +0.69, AL +0.64, DORM +0.56, FANG +0.36, INSP +0.35, PLMR +0.28, SNDX +-0.28, TDW +0.22, CE +0.19, TALO +0.16, AMRC +0.14, F +0.14, BFAM +0.12 of note (> 0.10)

Misses: NBIX -0.46, PRAA -0.35, VRTX -0.19, EVER -0.12, CLX -0.10, ETD -0.08, DENN -0.01, CTRA -0.01 of note.

Flat: None of note.

Capital Raises:

IPOs For The Week: ALEH, EGG, OMSE, YB

New IPOs/SPACs launched/News: None of note.

IPOs Filed/Priced: None of note.

Secondaries Filed or Priced: None of note.

Notes Priced:

FOUR issued 10,000,000 shares of its new class of 6.00% Series A Mandatory Convertible Preferred Stock pursuant to a previously announced underwritten public offering.

Notes Files: None of note.

Convertibles Filed: None of note.

Direct Offering: None of note.

Exchangeable Subordinate Voting Shares: None of note.

Private Placements: None of note.

Selling Shareholders of note:

WGRX files for 3,578,254 share common stock offering by selling shareholder

Mixed Shelf Offerings:

ZEUS files for $200 mILLION mixed securities shelf offering

News After The Close:

Celanese (CE) announces its intent to divest its Micromax portfolio of products.

NASDAQ reports April volumes. (press release)

CBOE reports trading volume for April 2025. (press release)

Ford (F) to take a $2.5 billion charge on Tariffs of which $1 billion will be recouped making loss $1.5 billion.

Palantir (PLTR) falls despite strong earnings and guidance. (CNBC)

10K or Qs Filings/Delays – (Filed), (Delayed) None of note.

Exchange/Listing/Company Reorg and Personnel News:

NKE announces senior leadership changes to accelerate growth and drive win now action plan; Amy Montagne Becomes President, Nike.

WMB announced that effective July 1, 2025, President and CEO Alan Armstrong will become executive chairman of the Williams Board of Directors and Chad Zamarin, currently executive vice president of Corporate Strategic Development, will succeed him as president and CEO and will join the Williams board.

BOOT appoints John Hazen as CEO, effective May 5.

TDC appoints John Ederer as CFO, effective May 12.

ASH announces that CFO Kevin Willis has decided to leave Ashland to pursue another opportunity on May 16; co appoints William Whitaker as interim CFO until the board concludes its review process.

Buybacks: None of note.

Dividends Announcements or News:

Stocks Ex Div Today: None of note.

Stocks Ex Div Wednesday of note: None of note.

CBT increases quarterly dividend 5% to $0.45/share from $0.43/share.

CAH increases quarterly cash dividend to $0.5107/share from $0.5056/share.

Stocks Moving Up & Down After The Close:

Gap Up: TDUP +16.7%, AMRC +16.5%, SIBN +13.3%, NBIX +13%, UPWK +11.1%, TDW +9.7%, TALO +9.2% of note.

Gap Down: TCMD -21.1%, HSTM -13.2%, JELD -12.8%, ICHR -12.4%, PRAA -9.8%, BRBR -9.1%, PLTR -8.6%, CORT -7.5%, FN -6.7%, LSCC -5.6%, EVER -5.1%, MATX -5.1%, ETD -4%, HIMS -3.5%, VMEO -2.9%, VRTX -2.7%, F -2.6%of note.

What’s Happening This Morning: (as of 7:00 a.m. EDT)

Futures S&P 500 , NASDAQ , Dow Jones , Russell 2000 . Europe is lower and Asia is lower ex Japan. Bonds are at 4.351% from 4.318% yesterday on the 10-Year. Crude Oil and Brent Crude are higher with Natural Gas higher. Gold and Silver are higher with Copper lower. The U.S. Dollar is lower versus the Euro, lower against the Pound and lower against the Yen. Bitcoin is at $94,219 from $94,385 lower by $-314 (-0.33%).

Sector Action:

Daily Positive Sectors: Consumer Defensive of note.

Daily Negative Sectors: Energy, Consumer Cyclical, Technology and Financials of note.

One Month Winners: Communication Services, Technology, Consumer Defensive, Industrials and Utilities of note.

Three Month Winners: Consumer Defensive and Utilities of note.

Six Month Winners: Financials, Consumer Defensive, Communication Services and Utilities of note.

Twelve Month Winners: Financials, Communication Services, Utilities, Technology, Consumer Defensive, Real Estate and Consumer Cyclical of note.

Year to Date Winners: Consumer Defensive, Utilities, Materials and Financials of note.

Bolded means the Sector is new to the period in which it falls.

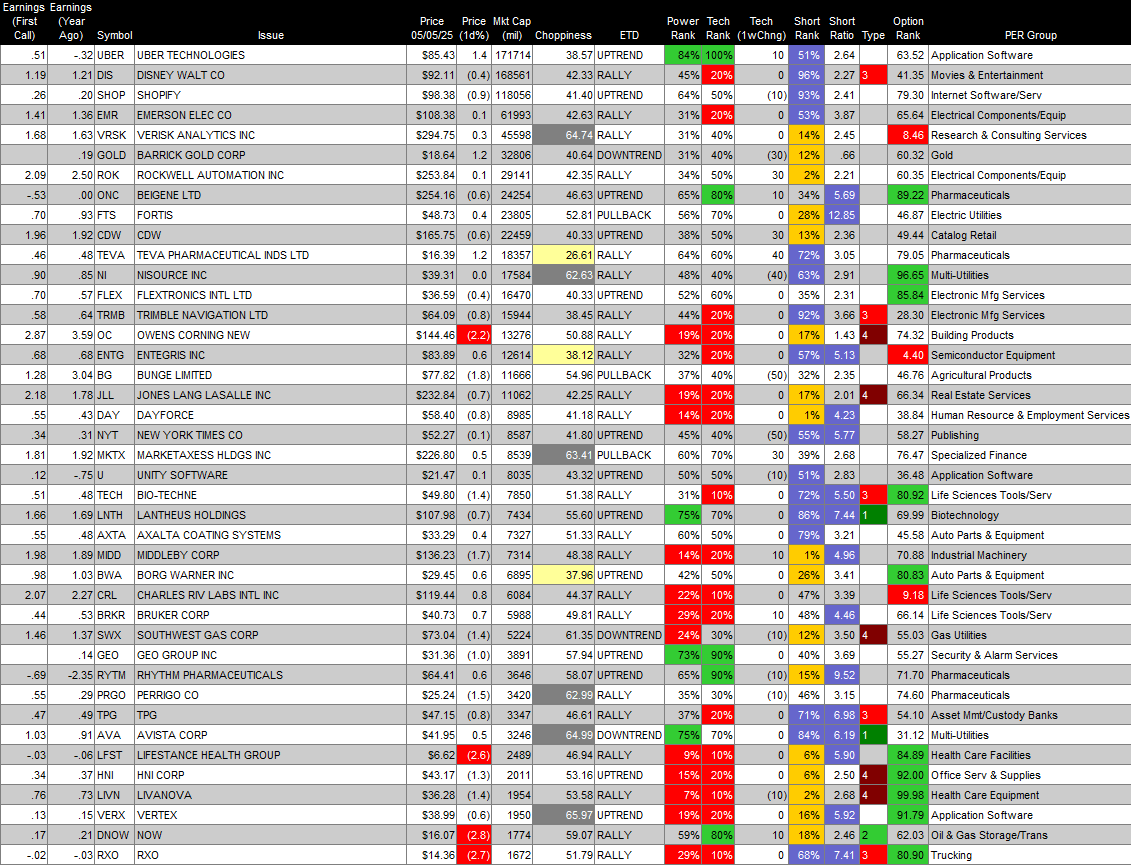

Upcoming Earnings Of Note: (From Chartroom Software – sorted by market cap, highest to lowest with most visible names)

Tuesday After the Close:

Wednesday Before The Open:

Notable Earnings of Note This Morning:

Flat: None of note

Beats: LCII +0.63, ACLS +0.49, LDOS +0.47, LEA +0.43, MPC +0.30, IT +0.26, DUK +0.16, AEP +0.14, GPN +0.14, KBR +0.12, DCO +0.13 of note. (>than 0.10)

Misses: THS -0.47, JJSF -0.30, RACE -0.21, BEAM -0.06, CEG -0.03, FWRG -0.04 of note.

Still to Report: None of note.

Company Earnings Guidance:

Positive Guidance: KNF EVER MWA NHI NJR PLTR PAY of note.

Negative or Mixed Guidance: CBT ICHR of note.

Advance/Decline Daily Update: The A/D crossed above its 30-day exponential moving average last week.

Gap Ups & Down In Early Pre-Market: (+2% or down more than -2%):

Gap Up: TDUP +23.6%, AMRC +15.1%, UPWK +13.3%, IPI +13.1%, SIBN +12.7%, WRD +11.7%, PONY +11.3%, NBIX +11.3%, LMND +9%, TALO +8.3%, TDW +8.1%, AESI +7.9%, TTAM +7.8%, CERT +7.4%, RRX +5.8%, CE +5%, OGS +4.8%, AVNT +4.7%, ERO +4.1%, VVX +4%, STRL +3.8%, WEAV +3.7%, BWXT +3.3%, AU +3%, CIB +2.9%, VAL +2.7%, CRBG +2.5%, ARAY +2.2%, VNOM +2.1%, SPNT +2.1% of note.

Gap Down: TCMD -22.5%, JRVR -20.4%, ICHR -15.9%, HSTM -14.4%, JELD -13.1%, PRAA -10.9%, ALDX -10%, PLTR -9.1%, CSTL -7.7%, SNDX -7.4%, CELH -7.1%, FN -6.5%, MD -6.5%, HIMS -6%, CORT -5.2%, NMFC -5.2%, EVER -5.1%, BRBR -4.8%, VRTX -4.8%, WGRX -4.6%, CBT -4.5%, PHG -4.2%, MATX -3.5%, CLX -3.2%, CRH -3.1%, AROC -3%, SHLS -2.9%, VMEO -2.9%, PDM -2.8%, KNF -2.8%, BCC -2.7%, CANG -2.5%, DENN -2.4%, ETD -2.2%, F -2.2%, KRC -2.1% of note.

Insider Action: None of note sees Insider Buying with dumb short selling. None of note see Insider Buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

Bloomberg: China's Firm Hand Restores Calm After Wild Asian Currency Moves. (Bloomberg)

Market Wrap: US Stocks Futures Drop on Signs of Trade War Damage. (Bloomberg)

Doordash (DASH) announces $1.2 billion SevenRooms Deal, misses on reveues. (CNBC)

Bloomberg Odd Lots: Brad Stetser on Taiwan Dollar Surge. (Podcast)

Bolded on story link means behind a Pay Wall.

Economic & Geopolitical:

Federal Reserve Speakers of note today.

Fed Speakers are back in Blackout period until this week's FOMC meeting is concluded.

Economic Releases:

March Trade Balance is out at 8:30 a.m. EDT and expected to drop to $-127.5 billion.

President Trump's Daily Schedule.

President Trump meets with the Canadian Prime Minister at 11:30 a.m. EDT.

President Trump participates in a FIFA Task Force Meeting at 3:30 p.m. EDT.

President Trump participates in a swearing in ceremony for the Assistant to the President, Senior Adviser and Special Envoy at 5:00 p.m. EDT.

M&A Activity and News: None of note.

Moving Average Table: Moves from 80% to 77% on Equity Indexes. Fixed Income (bonds) is back to struggling.

Meeting & Conferences of Note:

Sellside Conferences:

Davidson Financial Institutions Conference

Bloom Burton & Co. Healthcare Investor Conf

Morgan Stanley Healthcare Private Company

Oppenheimer Industrial Growth Conference

Stifel Investor Summit at WasteExpo

Wells Fargo Real Estate Securities Conference

Shareholder Meetings: None of note.

Top Analyst, Investor Meetings: None of note.

Fireside Chat: None of note.

R&D Day: None of note.

FDA Presentation: None of note.

Industry Meetings or Events:

Digestive Disease Week

EAS Congress

Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations.

Upgrades: MYPS SCSC UBS of note.

Downgrades: CVX FTNT MARA of note.