QPI Morning Note -9/19/24: Futures Are “El Fuego” Thanks To Doves Crying

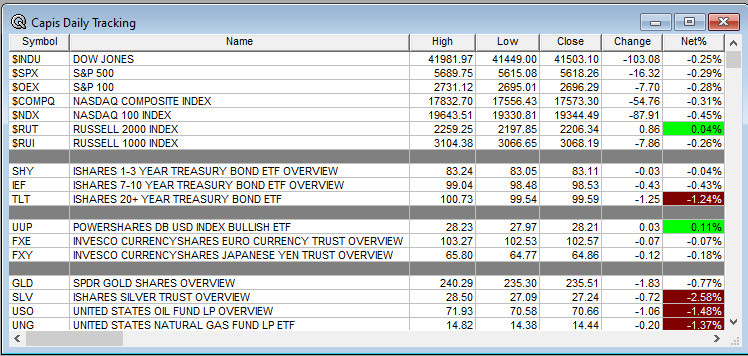

Overnight Summary: The S&P 500 closed Wednesday lower by -0.29% at 5618.26 from Tuesday higher by 0.03% at 5634.58. The overnight high was hit at 5774.74 at 6:35 a.m. EDT and the low was hit at 5686 at 4:05 p.m. EDT. The overnight range is 88 points. The current price is 5773.25 at 6:55 a.m. EDT higher by +93.25 points.

Most Important Article Of the Morning: Harris Had A Stronger Debate Than Trump But Race Remains Deadlocked (NYT)

Executive Summary: Stocks are “el fuego” this morning as we get back to life post FOMC. The move this morning is impressive especially after yesterday’s “give up” of the initial gains after the FOMC announcement and presser. I told a client after the close that we needed to see how today played out and glad that I provided that viewpoint.

Several Economic Releases of note today including Philly Fed, Existing Home Sales and Leading Indicators as well as Weekly Jobless Claims.

10-Year Tips Auction at 1:00 p.m. EDT.

Earnings Out After The Close:

Beats: SCS +0.02 of note.

Flat:

Misses: None of note.

Capital Raises:

IPOs For The Week: AAM, CUPR, DTSQ, FLAI, IBO, KAPA, VTRO

New IPOs/SPACs launched/News:

IPOs Filed/Priced:

Secondaries Filed or Priced:

ASND commences $300 mln ADS offering

AHR commences public offering of 14,500,000 shares of its common stock

CRMT announces that it intends to offer $65.0 mln shares of common stock in underwritten public offering

AHR – Primary Public Offering of Common Stock – 14,500,000 shares

EFSH: Form S-1.. $12.0 million Offering

VVOS – Pricing of $4.3 Million Registered Direct Offering of Common Stock Priced At-The-Market

Notes Priced:

Direct Offering:

Exchangeable Subordinate Voting Shares:

Selling Shareholders of note:

HESM announces commencement of public offering of 10.0 mln Class A shares by an affiliate of Global Infrastructure Partners

CTGO files for 1,698,887 shares of common stock offering by selling shareholders

Debt/Credit Filing and Notes:

Mixed Shelf Offerings:

ASNS files a $50 million mixed-shelf offering

ASND files mixed-shelf offering

EQH files a $800 million mixed-shelf offering

HE files mixed-shelf offering

PIPE:

Convertible Offering & Notes Filed:

Capital Raise Summary From The TradeXchange, bringing traders and investors real time news and Squawk Box, and other sources.

Biggest Movers Up & Down After The Close:

Movers Up: FDMT +4%, PLTK +2.9%, TRIB +2.7%, INCY +2.2%

Movers Down: PGNY -23.3%, CRMT -12.3%, SCS -10.2%, ASND -4.2%, AHR -3.4%

News After The Close :

PLTK enters into definitive agreement to acquire SuperPlay for $700 mln and additional contingent consideration of up to $1.25 billion

RGEN timing recognition of product revenue not recognized appropriately; financial statements require restatement; increases FY24 revenue guidance. No impact on revenues just on the quarters where revenues were reported with some “over” and some “under” stated.

PLTR awarded $99.8 mln U.S. Army contract for user licenses for the Maven Smart System AI tool

Several banks have announced 50 bps cuts to their prime lending rates following the Fed decision today: ASB, CFG, FITB, HBAN, KEY, NTRS, RF, SAN, USB

10-Q or 10-K Delays – None of note.

NASDAQ Delisting Notice – None of note.

Buybacks or Repurchases: Buybacks should be slow as most companies are in a blackout period as earnings season kicks into gear.

None of note

Exchange/Listing/Company Reorg and Personnel News:

AIG announces that Keith Walsh will join company as Executive Vice President and Chief Financial Officer, effective October 21, 2024

SMAR COO Stephen Branstetter to resign, effective today; will serve as advisor through November 18; SMAR eliminating the position

AMKR announces that James Kim will be stepping down as Executive Chairman and retiring from the company, effective October 31

LZ Chief Technology Officer and Chief Product Officer resigned to pursue other opportunities

Dividends Announcements or News:

Stocks Ex Div Today: AVGO HPE BBY UWMC SNV ASO KFY VAC KLIC ELME FDUS SWBI

Stocks Ex Div Tomorrow: RCL VST IFF OMC DKS ALLE FAF MAIN PLTK ROIC LTC ALEX

AGX increases quarterly cash dividend 25% to $0.375 a share from $0.30 a share

What’s Happening This Morning: Futures S&P 500 +94 NASDAQ 100 +434 Dow Jones +511 Russell 2000+71. Asia is higher with Europe is higher this morning. VIX Futures are at 17.72 from 18.42 yesterday while Bonds are at 3.717% from 3.685% on the 10-Year. Crude Oil and Brent are higher with Natural Gas lower. Gold, Silver and Copper higher for a second day in a row. The U.S. Dollar is lower versus the Euro, lower versus the Pound and lower against the Yen. Bitcoin is at $62,905 from $59,757 higher by +4.31% this morning.

Sector Action – (1/3/6/12/YTD Updated Weekly with Monday release):

Daily Positive Sectors: Communication Services of note.

Daily Negative Sectors: All others weak lead on the downside by Utilities, Technology and Consumer Defensive of note.

One Month Winners: Real Estate, Utilities, Consumer Defensive, Financials, Consumer Cyclicals and Industrials of note.

Three Month Winners: Real Estate, Utilities, Financials, Consumer Defensive, Healthcare and Industrials of note.

Six Month Winners: Utilities, Consumer Defensive, Real Estate, Technology, Financials and Communication Services of note.

Twelve Month Winners: Technology, Financials, Communication Services, Industrials, Utilities and Healthcare note.

Year to Date Winners: Technology, Utilities, Financials, Communication Services, Consumer Defensive and Healthcare of note.

Upcoming Earnings Of Note: (From Chartroom Software – sorted by market cap, highest to lowest with most visible names)

Thursday After the Close:

Friday Before The Open: None of note

Earnings of Note This Morning:

Beats: FDS +0.12 note.

Flat:

Misses: CBRL -0.10, DRI -0.08 of note.

Still to Report: DAVA

Company Earnings Guidance:

Positive Guidance: None of note.

Negative or Mixed Guidance: None of note.

Advance/Decline Weekly Update With Both Daily and Weekly Stats: Markets have improved nicely in the last week. The Daily A/D Line has made a new high while the S&P 500 has yet to. A bit of a divergence currently but that may be over today as Futures are “el fuego” and should take out the July high.

Gap Ups & Down In Early Pre-Market (+2% or down more than -2%):

Gap Up: ALGS +11.7%, NBTX +11%, TRIB +6%, PLUG +5.2%, PHI +5%, FDMT +4%, AMKR +3.9%, PLTR +2.5%, VST +2.2%, GOOG +1.9%

Gap Down: PGNY -28%, CRMT -11.9%, SCS -7.9%, HESM -3%, AHR -1.8%

Insider Action: WSC sees Insider buying with dumb short selling. None of note see Insider buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

What You Need To Know to Start Your Day. (Bloomberg)

5 Things To Know Before The Market Opens. (CNBC)

Pre-Market Movers: DRI DASH NVDA NEE COUR (CNBC)

Bloomberg Lead Story: NASDAQ Jumps 2% as Big Fed Cut Spurs Rally. (Bloomberg)

Markets Wrap: See lead story. (Bloomberg)

The man who made Nike (NKE) uncool, current CEO John Donahoe. (Bloomberg)

Darden (DRI) sees fine dining struggle. (CNBC)

Bloomberg: The Big Take – Xi unleashes a crisis of China’s best-paid workers. (Podcast)

Bloomberg: Odd Lots – The next stage of the credit cycle. (Podcast)

NY Times Daily: The Day the Pagers Exploded. (Podcast)

Economic:

September Philadelphia Fed Index is due out at 8:30 a.m. EDT and expected to rise to 3.0 from -7.0.

August Existing Home Sales is due out at 10:00 a.m. EDT and expected to fall to 3.90 million from 3.95 million.

At the same time, August Leading Indicators are expected to remain in the negative at -0.3% from -0.6%.

Weekly Jobless Claims are due out at 8:30 a.m. EDT.

Weekly Natural Gas Numbers are due out at 10:30 a.m. EDT.

Geopolitical:

President Biden receives the Daily Briefing at 10:00 p.m. EDT.

President Biden to give a speech at the Economic Club of Washington at 1:15 p.m. EDT

Press Briefing by Press Secretary Karine Jean-Pierre and Chairman of the Council of Economic Advisors Jared Bernstein

President Biden delivers remarks to the Congressional Hispanic Caucus Institute 47th Annual Awards Gala at 8:45 p.m. EDT

Federal Reserve Speakers:

Blackout period is now over.

M&A Activity and News:

PLTK enters into definitive agreement to acquire SuperPlay for $700 mln and additional contingent consideration of up to $1.25 billion

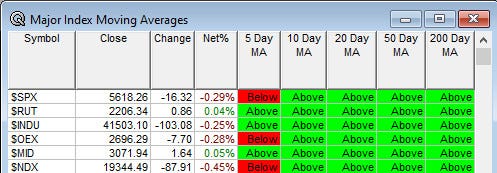

Moving Averages On Major Indexes: Move from 100% to 90% of the moving averages being positive.

Meeting & Conferences of Note:

Sellside Conferences:

Bank of America Global Healthcare Conference

Cantor Fitzgerald Global Healthcare Conference

Craig-Hallum Bioprocessing Conference

D. A. Davidson Diversified Industrials & Services Conference

Janney Virtual Water Utilities Conference

Sidoti Small Cap Conference

TD Securities Forest Products and Packaging Conference

Wells Fargo Consumer Conference

Fireside Chat: None of note.

Top Shareholder Meetings: KUKE, MASI, STRM

Investor/Analyst Day/Calls: AJG, ALTM, CAE, CDZI, GLW, PX, TMO, UNP

Update: None of note.

R&D Day: None of note.

FDA Presentation:

Company Event:

Industry Meetings or Events:

IoT Developer Conference

ASNE Fleet Maintenance & Modernization Symposium

European Committee for Treatment and Research in Multiple Sclerosis

LABScon: The Ultimate Cybersecurity Research Conference

Space Education and Strategic Applications (SESA) Virtual Conference

TOKEN2049 Singapore

Top Tier Sell-side Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from QPI or its employees.

Upgrades: PRLD DASH

Downgrades: MUSA FIVE CASY