QPI Morning Note - 11/6/24: Trump Beats Harris. Republic Take The Senate With House Likely To Remain in Their Control. Futures Higher.

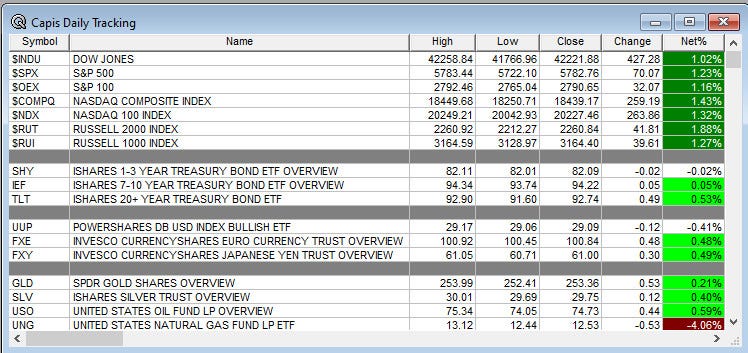

Overnight Summary: The S&P 500 closed Tuesday higher by 1.23% at 5782.76 from Monday lower by -0.28% at 5712.69. The overnight high was hit at 5954 at 3:50 a.m. EDT and the low was hit at 5814.25 at 4:05 p.m. EDT. The overnight range is 140 points. The current price is 5937.50 at 7:20 a.m. EDT higher by +125.25 points higher by +2.15%.

Executive Summary: Well the people voted and their voices were heard. As the rock band The Who sings, “Meet the new boss, same as the old boss.” Ironically, that line is from the song “Won’t Get Fooled Again.” I am seeing lots of comments on social media proclaiming broken hearts, the U.S. is toast and that we are going back to a repressive period. Give it some time. See how this shakes out. The United States is still that city on the hill that Ronald Reagan described what is now a long time ago.

Article of Note:

Key Events of Note Today:

Economic releases of note today include Weekly Crude Oil Inventories. Weekly Mortgage Applications fell -10.80%.

At 1:00 p.m. EDT, the Treasury holds a 30 -Year Note Auction.

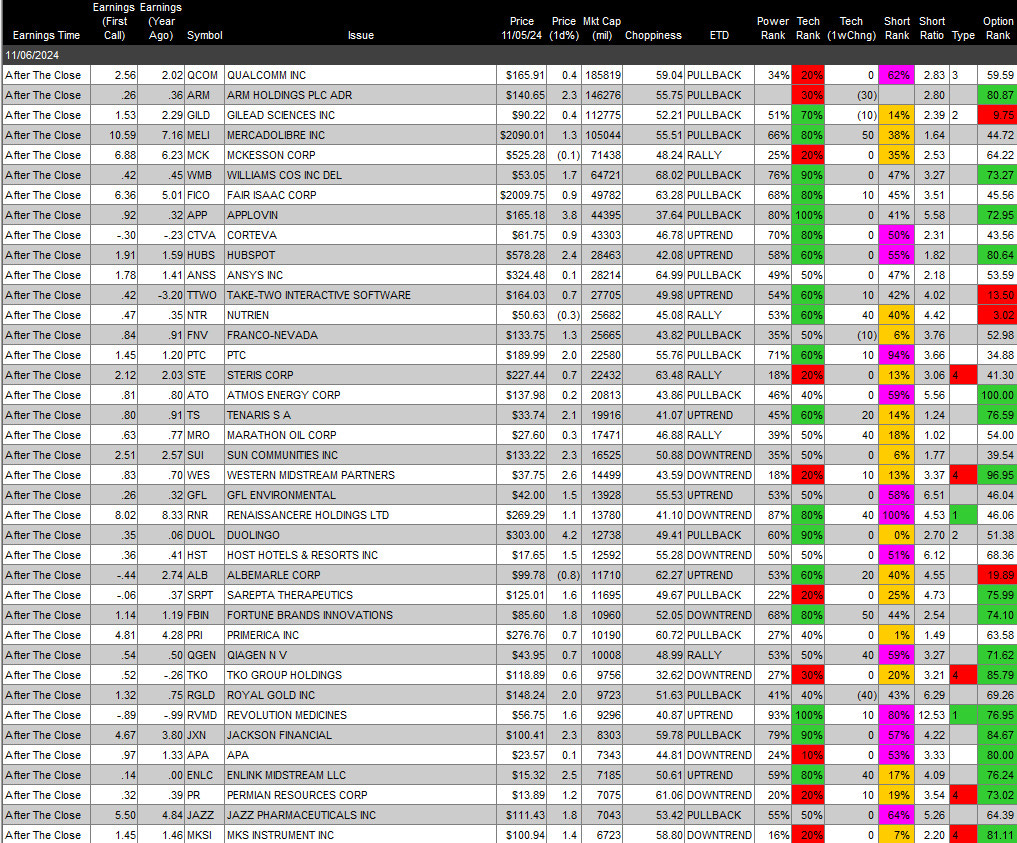

Earnings Out After The Close

Beats: QLYS +18.6%, RVLV +15.6%, TMCI +14.1%, MGNX +12.2%, GMED +9.5% of note.

Flat: None of note.

Misses: EXAS -30.1%, AVNW -18.2%, MEC -17.1%, SMCI -15%, CPNG -8.8% of note.

Capital Raises:

IPOs For The Week: ADUR, ALEH, CASK, CGTL, HIT, JUNS, LEC, MSW, PHH, WYHG

New IPOs/SPACs launched/News:

IPOs Filed/Priced:

Secondaries Filed or Priced:

ERNA: Form S-1.. Up to 49,870,566 Shares of Common Stock

Notes Priced:

Direct Offering:

Exchangeable Subordinate Voting Shares: None of note.

Selling Shareholders of note:

Mixed Shelf Offerings:

ANAB files $500 mln mixed shelf securities offering

LMB files mixed shelf securities offering

AMST: Form S-3, $100,000,000. Mixed Shelf

PIPE:

PLBY Group (PLBY) completes $22.35 million Private Placement

ZCAR pricing of $9.15 million Private Placement

Convertible Offerings & Notes Filed:

Capital Raise Summary From The TradeXchange, bringing traders and investors real time news and Squawk Box, and other sources.

Biggest Movers Up & Down After The Close:

Movers Up: QLYS +18.6%, RVLV +15.6%, TMCI +14.1%, MGNX +12.2%, GMED +9.5% of note.

Movers Down: EXAS -30.1%, AVNW -18.2%, MEC -17.1%, SMCI -15%, CPNG -8.8% of note.

News After The Close:

CBOE reports trading volume for October 2024. (Press Release)

iRobot (IRBT) will implement an operational restructuring plan

FTC takes action against online cash advance app Dave (DAVE) for “deceiving consumers, charging undisclosed fees” .

WillScot Mobile Mini (WSC) spiking by +7% after TOMS Capital Investment Management builds stake in the company, pushes for a strategic review. (Bloomberg)

Cisco (CSCO) routers, among others, were used by hackers in Chinese intrusions. (WSJ)

Super Micro Computer (SMCI) remains unable at this time to predict with its Form 10-K will be filed. (CNBC)

Spirit Aerosystems (SPR) in 10-Q filing warns substantial doubt about its ability to continue as a going concern exist. (Reuters)

10-K Delays – SMCI

Barron’s: Sweeping changes are coming to Washington and beyond. (Barron’s)

Buybacks or Repurchases:

GPOR expands Common Stock Repurchase Authorization by 54% to $1.0 billion

CMA approves the authorization to purchase up to an additional 10 million shares of Comerica Incorporated outstanding common stock

Exchange/Listing/Company Reorg and Personnel News:

MRC announces that its board of directors has elected Deborah G. Adams as its new Board Chair, effective immediately.

GBCI appointed Ryan Screnar to serve as an Executive Vice President and Chief Compliance Officer

Dividends Announcements or News:

Stocks Ex Div Today: SCCO BRO EQT WFRD NEP AROC VSEC GBX WT UVSP HFWA

Stocks Ex Div Tomorrow:

TXO increases quarterly distribution to $0.58/share from $0.57/share.

What’s Happening This Morning: Futures S&P 500 + NASDAQ + Dow Jones + Russell 2000 + (at 8:25 a.m. EDT). Asia is higher and Europe is higher. VIX Futures are at 16.20 from 18.59 yesterday while Bonds are at 4.47% from 4.327% on the 10-Year. Crude Oil and Brent are lower with Natural Gas higher. Gold, Silver and Copper lower for the first time in four days. The U.S. Dollar is higher versus the Euro, higher versus the Pound and higher against the Yen. Bitcoin is at $74,433 from $68,821 higher by +$4,988 up 7.20% this morning.

Sector Action – (1/3/6/12/YTD Updated Weekly with Monday release):

Daily Positive Sectors: Utilities, Industrials and Consumer Cyclicals of note.

Daily Negative Sectors: None of note.

One Month Winners: Financials, Communication Services, Technology and Consumer Cyclicals of note.

Three Month Winners: Consumer Cyclicals, Technology, Financials, Communication Services of note.

Six Month Winners: Technology, Utilities, Real Estate, Financials and Communication Services of note.

Twelve Month Winners: Technology, Financials, Utilities, Communication Services and Industrials note.

Year to Date Winners: Technology, Utilities, Financials, Industrials and Communication Services of note.

Upcoming Earnings Of Note: (From Chartroom Software – sorted by market cap, highest to lowest with most visible names)

Wednesday After the Close:

Thursday Before The Open:

Earnings of Note This Morning:

Beats: LINE +2.16, JLL +0.76, ATHM+0.39, OC +0.33, CRL +0.17, IONS +0.17, HWM +0.16, DIN +0.10, IRBT +0.09, EYE +0.06, AEP +0.05, KMT +0.03, TEVA +0.03, IRM +0.02 of note.

Flat: None of note.

Misses: SMG-0.35, CVS -0.35, BCO -0.28, SRE -0.18, SWX -0.07, VSH -0.06, PFGC -0.06, CELH -0.02, MAC -0.01 of note.

Still to Report:

Company Earnings Guidance:

Positive Guidance: of note.

Negative or Mixed Guidance: of note.

Advance/Decline Daily Update: The A/D Line had a nice pop yesterday that should continue today.

Gap Ups & Down In Early Pre-Market (+2% or down more than -2%):

Gap Up: DJT +36.8%, QLYS +20.2%, RVLV +17.9%, MGNX +14.9%, TMCI +14.1%, MRCY +13.4%, GMED +12.6%, CMA +9%, IWM +6.4%, RYAM +6.3%, JKHY +6.2%, WSC +6.1%, LMB +5.4%, MASI +5.2%, CMC +4.6%, TSLX +4.6%, OC +4.4%, WFRD +4.3%, PCVX +4.1%, NOG +3.8%, EMR +3.7%, DAVE +3.6%, CRC +3.6%, AIZ +3.4%, ENOV +3%, DIA +2.9%, FUN +2.9%, AZPN +2.5%, SPY +2.3%, CRWD +2.2%, AFG +2.2%, NVO +2.1%.

GapDown: EXAS -27.3%, SMCI -23.4%, PACS -22.2%, AVNW -18.3%, EOSE -13.8%, MEC -13.1%, BGS -10.9%, BBAI -10.2%, SWIM -9.6%, IRBT -9%, CLVT -8.3%, LUMN -8%, MRC -8%, INNV -7.7%, HMC -7.5%, AUDC -7.2%, CPNG -6.1%, MBC -4.7%, CELH -4.7%, STKL -4.1%, CBOE -3.4%, NCMI -3.4%, VTEX -3.2%, WTTR -2.9%, LXRX -2.5%, NVAX -2.4%, MCHP -2.1%, ASR -2%, ERO -2%

Insider Action: HII sees Insider buying with dumb short selling. No names sees Insider buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

Pre-Market Movers: Yet to report. (CNBC)

5 Things To Know Before The Market Opens. (CNBC)

Bloomberg Lead Story: Donald Trump Wins US Presidency For A Second Time. (Bloomberg)

Markets Wrap: US Stocks, Dollar rally with Trump wins election. (Bloomberg)

Election Maps and Results. (Bloomberg)

PG&E (PCG) cuts power to 25,000 on risk of wildfires. (Bloomberg)

10-year yield jumps above 4.40%. (CNBC)

Novo Nordisk (NVO) jumps 8% on Wegovy sales beat estimates. (CNBC)

Bloomberg: Big Take – Trump’s Populism Unleashed. (Podcast)

Marketplace: Donald Trump wins the White House. (Podcast)

NY Times The Daily: Trump, Again. (Podcast)

Economic:

Weekly Mortgage Applications fell -10.80% from -0.01% last week. Mortgage rate goes to 6.81% versus 6.73%.

Weekly Crude Oil Inventories due out at 10:30 a.m. EDT.

Geopolitical:

Federal Reserve Speakers are in a blackout period due to FOMC meeting until Thursday.

President Biden receives the Daily Briefing at 1:30 p.m. EDT

A quiet day ahead as it is all about voting.

Watch our Twitter feed, Bullet86, for any impromptu appearances.

M&A Activity and News:

Aspen Tech (AZPN) announces receipt of unsolicited acquisition proposal from Emerson (EMR) to acquire all of the outstanding shares of common stock of the Company not already owned by Emerson for cash consideration of $240/share.

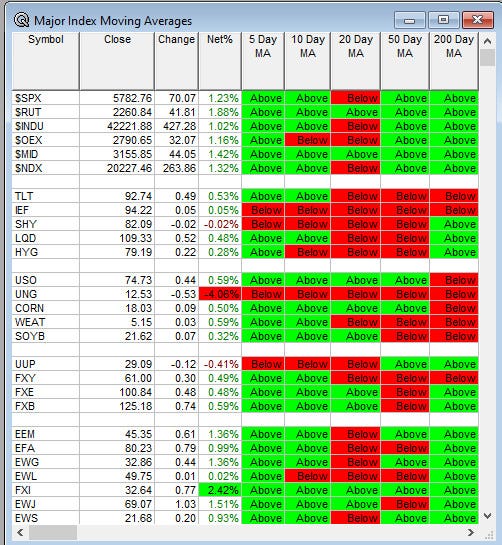

Moving Averages On Major Equity Indexes: Moves from 37% positive to 84%. Other asset classes saw some improvement.Bonds look to continue weakness.

Meeting & Conferences of Note:

Sellside Conferences:

Goldman Sachs APAC Healthcare Corporate Day

BAC Mexico Year Ahead Conference

Hovde Group Financial Services Conference

Jefferies Offshore Wind Contractors Summit

Fireside Chat: None of note.

Top Shareholder Meetings: ADP, ADTX, BITF, CAH, CLDI, GNPX, HRB, IMNN, LANC, RCUS, RLYB, SRRK, TBNK

Top Analyst, Investor Meetings: VTMX

Update: None of note.

R&D Day: None of note.

FDA Presentation:

Company Event: None of note.

Industry Meetings or Events:

Top Tier Sell-side Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from QPI or its employees.

Upgrades: SNOW CE

Downgrades: OSCR FIVE SMCI CBOE

Exec Summaryon this sunny but dismal morning was good, balanced commentary.