QPI Daily Note - 3/28/24: Q1 Is Over Today And It Was Epic! Q1 Earnings Start in 2-3 Weeks

Overnight Summary: The S&P 500 closed Wednesday higher by 0.86% at 5248.49 from Tuesday lower by -0.28% at 5203.58. The overnight high was hit at 53138.75 at 4:05 p.m. EDT while the overnight low was hit at 5301 at 5:30 a.m. EDT. The range overnight is 13 points as of 6:40 a.m. EST. The 10-day average of the overnight range is at 20.12 from 20.48. The average for May-January average was 20.88 from 20.87 during May-December. Currently, the S&P 500 is lower by -0.75 points at 6:40 a.m. EDT.

Executive Summary: Today is the last day of an epic quarter as the S&P 500 is up 10% and the best quarter in over a decade. Meanwhile, secondary and tertiary stocks were up much less, Russell 2000 was up 4.30%. Will next quarter be the small-cap quarter?

Q4 GDP (Final) is due out at 8:30 a.m. EDT and is expected to stay at 3.2%.

March Chicago PMI is due out at 9:45 a.m. EDT and is expected to improve to 45.4 from 44 in February.

University of Michigan Consumer Sentiment (Final) is due out at 10:00 a.m. EDT and expected to come in a 76.50 unchanged.

February Pending Home Sales are also due out at 10:00 a.m. EDT and expected to rise to 2.1% from -4.90%.

Earnings Out After The Close:

Beats: JEF +0.12, VRNT +0.10, FUL +0.03, CXM +0.03, BRZE +0.01, MLKN +0.01 of note.

Misses: RH (0.95), CC (0.35) of note.

Capital Raises:

IPOs Priced or News:

Boundless Bio (BOLD) (Nasdaq) prices 6.25 million share IPO at $16.00 per share, at the midpoint of the $15-17 expected range.

Alta Global Group Limited (MMA) Announces Pricing of Initial Public Offering.

Secondaries Priced:

PRAX: Prices $200 million public offering.

SNX: Prices secondary offering of 10.5 mln shares of common stock and concurrent share repurchase.

STOK: Prices upsized $125 million public offering.

Common Stock filings/Notes:

ATS: Announces C$163 million secondary offering of common shares at a price of C$46.55 per share.

FSBC: Launch of Common Stock Offering.

NCNA: Plan to Implement ADS Ratio Change.

PRAX: Announces proposed public offering of common stocks.

SNX: Proposes 9,000,000 shares secondary offering; concurrent buyback.

Selling Shareholders of note:

FET: Files for 1,946,038 shares of common stock by selling shareholders.

PYXS files for 10,460,586 shares of common stock by selling shareholders.

Mixed Shelf Offerings:

ABOS: Files $200 million mixed shelf securities offering

LUNR: Files $300 million common stock offering; also files for 159,808,031 shares of common stock by selling shareholders, relates to warrants.

SKYH: FORM S-3 - $200,000,000 Mixed Shelf Offering.

Capital Raise Summary From The TradeXchange, bringing traders and investors real time news and Squawk Box, and other sources.

News After The Close :

After Hours Movers:

AVTX: +250% Acquires Anti-IL-1β mAb and Announces Private Placement Financing of up to $185 Million

DPRO: +14% Earnings

VERU: +11% Initiated OUTPERFORM @ RJ

RH: +8% Earnings

ZCAR: +4.5% Partners with ACKO Drive

MLKN: -13% Earnings

PRAX: -5.5% Proposed Public Offering

SNX: -3% Launch of Secondary Public Offering of Common Stock and Concurrent Share Repurchase

News Items After the Close:

Hawaiian Holdings (HA) and Alaskan Airlines (ALK) enter into timing agreement with DOJ; have been working cooperatively with DOJ surrounding previously announced merger.

UnitedHealth Group (UNH) has paid more than $3 billion to providers following cyberattack to Change Healthcare. (CNBC)

Keysight (KEYS) to launch $1.45 billion rival offer for London-listed Spirent, Sky News reports. (Reuters)

Federal Reserve Board of Governors Christopher Waller: Speech Titled "There's Still No Rush"

Recent data warrants a no rush to cutting rates in current Economy -- warrants fewer cuts or a later start for lowering rates

Lockheed Martin (LMT) awarded $440 million U.S. Navy contract.

Goldman has a big macro take on autos this am: “.. Global EV uptake is at a turning point. .. our bear scenario calling for a y/o/y decline in EV sales volume in 2024 has become more realistic. .. due to concerns about .. lower prices for used EVs, .. poor visibility on government policy, .. a shortage of rapid-charging stations. Under these circumstances, we clarify our relative preference for [hybrids].” (CQ CNBC)

Exchange/Listing/Company Reorg and Personnel News:

Index Changes: GE Vernova (GEV) and Solventum (SOLV) to join S&P 500; Dentsply Sirona (XRAY) to join S&P MidCap 400, V.F. Corp. (VFC), which will be moved to the S&P SmallCap 600

Ally Financial (ALLY) names Michael Rhodes as CEO.

Alpha Star Acquisition Corporation (ALSA) identified two classification errors made in certain of the previously issued financial statements; files to delay 10-K.

Carlyle Group (CG) COO Christopher Finn to retire, effective June 30; Deputy COO Lindsay LoBue to become COO.

Discover Financial Services (DFS) CEO Michael G. Rhodes to resign, effective April 1; J. Michael Shepherd appointed interim CEO upon Mr. Rhodes' resignation. (WSJ)

Eve Holding (EVEX) to delay 10-K filing.

FinWise Bancorp (FINW) appoints Jim Noone to President along with the hiring and appointment of Robert Wahlman as Chief Financial Officer.

SharkNinja (SN) announces that Patraic Reagan has been named Chief Financial Officer.

SilverBow Resources (SBOW) appoints Leland T. Jourdan to the Board of Directors; Christoph O. Majeske stepping down.

Buyback Announcements or News:

Autoliv (ALV) retired 1,370,057 shares of common stock that had been repurchased during the quarter which resulted in a decrease in the issued shares.

Erasca (ERAS) enters into a securities purchase agreement to sell 21,844,660 shares of common stock in an oversubscribed private placement at a price of $2.06 per share.

TD Synnex (SNX) see capital raises.

United Parks & Resorts Inc. (PRKS) shareholders approve $500 million buyback authorization and amended agreement with Hill Path Capital LP.

Stock Splits or News:

ODFL trading 2/1 today.

Reverse Split stocks today DOYU 1/10.

Dividends Announcements or News: None of note.

What’s Happening This Morning: Futures value reflects the change with fair value.

S&P 500 +2, Dow Jones +26, NASDAQ -10, Russell +5. (as of 7:56 a.m. EST). Asia is lower ex Australia while Europe is higher this morning. VIX Futures are at 14.11 from 14.20 this morning. Gold is higher with Silver and Copper lower this morning. WTI Crude Oil and Brent Crude Oil are higher with Natural Gas lower. US 10-year Treasury sees its yield at 4.22% from 4.224% this morning. The U.S. Dollar is higher versus the Euro, higher versus the Pound and higher against the Yen. Bitcoin is at $70.402 from $70,081 higher by +2.57% this morning..

Sector Action –

Daily Positive Sectors: Utilities, Real Estate, Basic Materials, Industrials, Healthcare, Financials of note.

Daily Negative Sectors: None of note.

Major stock indexes rose Wednesday, with the S&P 500 snapping a three-day slide to close at a record. The S&P 500 rose 0.9%, while the Dow Jones Industrial Average added 1.2% and the Nasdaq Composite closed 0.5% higher. The S&P 500 is little changed on the week but heading for a spectacular first quarter, currently up 10% year-to-date. The benchmark 10-year Treasury yield declined to 4.195% from 4.233% the prior day, reversing its recent climb. (WSJ - edited by QPI)

Upcoming Earnings Of Note:

Thursday After the Close: OXM, SMTC, SHCR, CURV of note.

Monday Before the Open: None of note.

Earnings of Note This Morning:

Beats: REX +0.45, WBA +0.38, ATAT +0.03, MSM +0.02 of note.

Misses: DOOO (0.14CAD) of note.

Company Earnings Guidance:

Positive Guidance: CTAS, RH of note.

Negative Guidance: UNF, MLKN, VNET, DOOO of note.

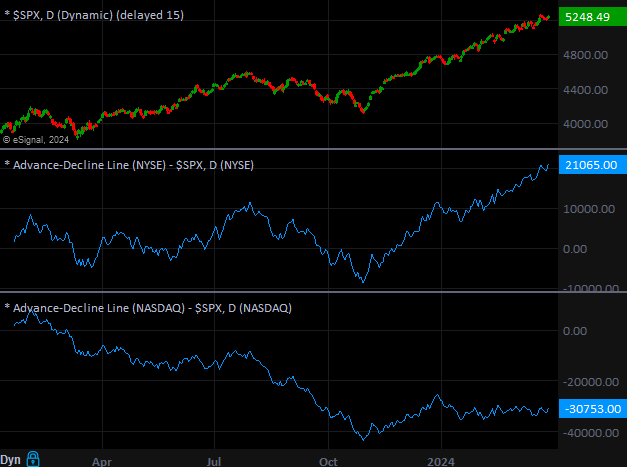

Erlanger Research Advance/Decline Chart:

Gap Ups & Down In Early Pre-Market (+2% or down more than -2%):

Gap Up: AKBA +19%, ERAS +13%, ABOS +12%, CXM +10%, RH +8%, RILY +6%, CWCO +4% of note.

Gap Down: MLKN -15%, CC -11%, FC -7%, SSP -5%, SNX -5%, LUNR -5%, RUM -4%, DOOO -4%, MODV -4% of note.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

5 Things To Know Before the Stock Market Opens Today. (CNBC)

What You Need To Know To Start Your Day. (Bloomberg)

Morning Briefing For Bloomberg Subscribers. (Bloomberg)

Stocks Making The Biggest Moves: WBA, EL, ALL, RH, SNX, CC, VNO (CNBC)

Bloomberg Lead Story: Bridge loss may trigger historic marine loss says Lloyd's of London. (Bloomberg)

Bonds fall and stocks hover on rate cute push back: Markets Wrap. (Bloomberg)

Walgreens (WBA) beats on revenues but narrows profit outlook. (CNBC)

Home Depot (HD) to buy distributor SRS in bid to increase pro sales. (CNBC)

Bloomberg: The Big Take: UBS bankers frustration exposes cracks in world of climate finance. (Podcast)

NYT The Daily: The newest tech billionaire, Donald J. Trump. (Podcast)

Marketplace: Government is jawboning Big Tech. (Podcast)

Wealthion: Looming retirement crisis. (Podcast)

Moving Average Update: Score improves to 97%.

Geopolitical:

President’s Public Schedule:

The President receives the President’s Daily Brief, 10:00 a.m. EDT

The President departs the White House en route Joint Base Andrews, 11:10 a.m. EDT

The President departs Joint Base Andrews en route John F. Kennedy International Airport, 11:40 a.m. EDT

Press Secretary Karine Jean-Pierre will speak aboard Air Force One en route Queens, New York, 12:00 p.m. EDT

The President arrives at John F. Kennedy International Airport, 12:35 p.m. EDT

The President departs John F. Kennedy International Airport en route the Wall Street Landing Zone, 12:45 p.m. EDT

The President arrives at the Wall Street Landing Zone, 1:00 p.m. EDT

The President and The First Lady participate in a campaign reception, 8:05 p.m. EDT

Economic:

Q4 GDP (Final) is due out at 8:30 a.m. EDT and is expected to stay at 3.2%.

Jobless Claims 8:30 a.m. EDT

Corporate Profits 8:30 a.m. EDT

March Chicago PMI is due out at 9:45 a.m. EDT and is expected to improve to 45.4 from 44 in February.

University of Michigan Consumer Sentiment (Final) is due out at 10:00 a.m. EDT and expected to come in a 76.50 unchanged.

Michigan Inflation Expectations 10:00 a.m. EDT

February Pending Home Sales are also due out at 10:00 a.m. EDT and expected to rise to 2.1% from -4.90%.

EIA Natural Gas Report 10:30 a.m. EDT

Baker Hughes Rig Count 1:00 p.m. EDT

Farm Prices 3:00 p.m. EDT

Federal Reserve / Treasury Speakers:

Saturday - March 29th 11:30 a.m. EDT - Federal Reserve Chair Jerome Powell

M&A Activity and News:

Capital Bancorp (CBNK) will acquire IFH (OTCQX: IFHI) in a cash and stock transaction valued at $66 mln exclusive of the value of a dividend to be received by IFH shareholders at or immediately prior to closing.

Progress Software (PRGS) confirms that any offer for MariaDB plc is likely to be solely in cash.

Take-Two (TTWO) acquires The Gearbox Entertainment Company for $460 million.

Meeting & Conferences of Note:

Sellside Conferences:

H.C. Wainwright Autoimmune and Inflammatory Disease Virtual Conference

Top Shareholder Meetings: GMFI, IMUX, JEF, JVA, LCTX, MATH, OPK, RNTX, TCN

Investor/Analyst Day/Calls: ED, GE, KOD, PPCB

Industry Meetings:

Immunic, Inc. Society for Virology Meeting

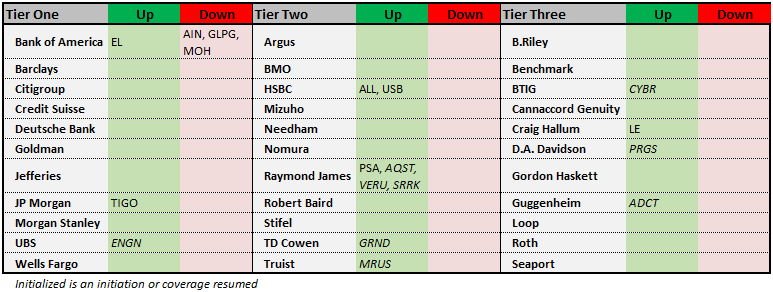

Top Tier Sell-side Upgrades & Downgrades: