Morning Note - 02/06/26: Stocks Bouncing Off Oversold, Ending A Terrible, Horrible, No Good Week For The Bulls

Overnight Summary & Early Morning Trading:

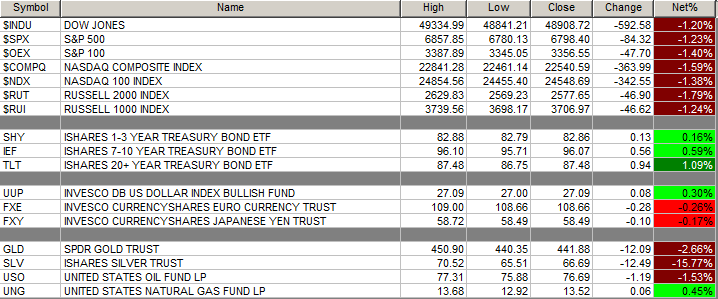

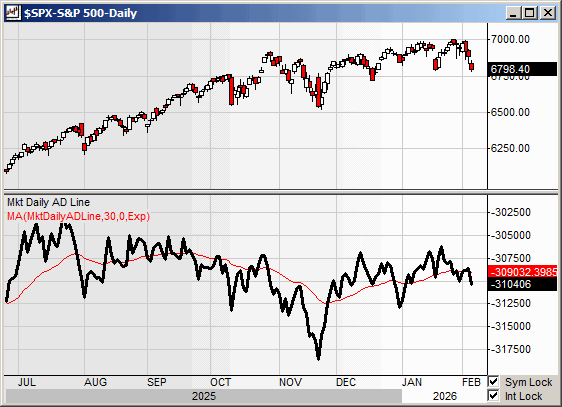

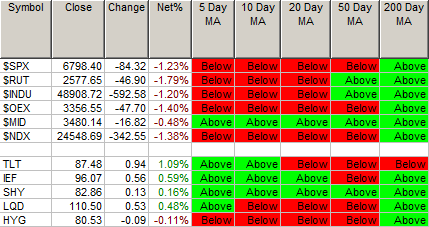

The S&P 500 finished Thursday lower by -1.23% at 6798.40 from Wednesday lower by -0.51% at 6882.79.

The S&P 500 sees support now at 6700 from 6800. Resistance is now at 6800 from 6900.

S&P 500 hit its fourth All-Time Closing High of 2026 last Tuesday, 1/27/26.

Year to date the S&P 500 is lower by -0.69% from 0.54% on yesterday’s close.

Futures are higher this morning by +38.50 (+0.60%) at 6859 on the SP 500 around 6:30 a.m. EST.

Bond Market is higher today on price with the 10-Year Yield at 4.20% from 4.282%.

Executive Summary:

Last week we noted that is was, “Highly unlikely that there was a cut with strong Q3 GDP and the Atlanta Fed’s forecast of 5.4% Q4 GDP”. That favored a selloff and yesterday we fell by -1.23%, so extended downside action is starting to become a trend.

This is another big earnings week. Volatility continues with positive moves in while there were big drops in .

Stocks sold off hard again on Thursday but did not recover their losses by the close, unlike Tuesday and Wednesday. So we are still in the Danger Zone.

Bitcoin back to $66,000 from $70,000 yesterday morning, but is higher from the low on Thursday. A bottom as opposed the “the bottom”.

Key Events of Note Today:

Economic news of note is still delayed due to the government shutdown but we will be producing what is scheduled to be reported.

Weekly - Baker Hughes Rig Count of note.

Monthly - University of Michigan Consumer Sentiment out at 10:00 a.m. EST. Consumer Credit at 3:00 p.m. EST.

Fed Speakers of Note today: None of note.

President Trump’s schedule:

Heads to Palm Beach this morning

Signs Executive Orders at 3:00 p.m. EST.

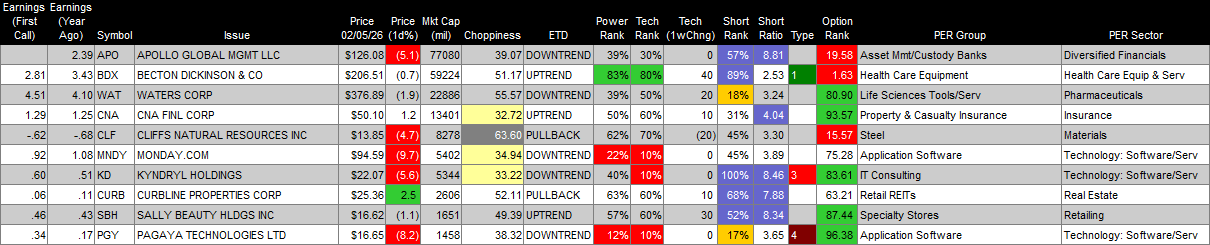

Notable Earnings Out After The Close: (Beats > $0.10)

Beats: RGA +1.97, MGM +0.94, ARW +0.79, VSAT +0.65, MTD +0.56, RDDT +0.30, BYD +0.27, PCTY +0.25, FLS +0.17, BE +0.14 and IREN+0.11 of note.

Misses: MSTR -42.85, MOH -3.09, CLSK -1.04, UNM -0.19, VRSN -0.12of note.

Flat: None of note.

Capital Raises:

IPOs For The Week: None of note.

New IPOs/SPACs launched/News: None of note.

IPOs Filed/Priced: None of note.

Secondaries Filed Or Priced:

CARR: Form S-3.. 50,074,109 Shares of Common Stock, Par Value $0.01 Per Share.

IMCC: Form F-3.. Up to 9,788,966 Common Shares.

IPSC: Form S-3.. 176,086,947 Shares of Common Stock.

MANE - Closing of Full Exercise of Underwriters’ Option to Purchase Additional Shares in Initial Public Offering.

Notes Filed Or Priced:

MPLX - prices $1.5 billion senior notes offering.

Convertible Offerings Filed or Priced: None of note.

Direct Offering: None of note.

Exchangeable Subordinate Voting Shares: None of note.

Selling Shareholders: None of note.

Private Placements: None of note.

Mixed Shelf Offerings:

JCI: FORM S-3ASR - Mixed Shelf Offering.

PHM: FORM S-3ASR - Mixed Shelf Offering.

News After The Close:

Amazon (AMZN) missed on earnings but beat on revenues and gave a higher CapEx number sending it lower.

Hub Group (HUBG) delays full earnings release and conference call; sees FY25 revs slightly above consensus and FY26 revs in line.

Exchange/Listing/Company Reorg and Personnel News: None of note.

Buybacks:

RDDT authorizes repurchase program of up to $1 billion of Class A common stock.

SPG may purchase up to $2.0 billion of its common stock through February 29, 2028, as market conditions warrant.

Dividends Announcements or News:

Stocks Ex Div Today of note: PH HWM FE JBHT SSB KNTK MAIN WTTR of note.

Stocks Ex Div Tomorrow of note: None of note.

KNSL increases cash dividend to $0.25 per share from $0.17 per share.

What’s Happening This Morning: (as of 7:35 a.m. EST)

Futures S&P 500 +35, NASDAQ 100 +150, Dow Jones +243. Europe is higher while Asia is mixed. Bond yield is at 4.20% from 4.264% on the 10-Year. Crude Oil and Brent Crude are lower with Natural Gas higher. Gold higher with Silver and Copper lower. The U.S. Dollar is lower versus the Euro, lower against the Pound and higher against the Yen. Bitcoin is at $66,185 higher by 4.17% up $2628$69.297 lower -5.56% down $-4067.

Sector Action:

Daily Positive Sectors: Consumer Defensive were higher.

Daily Negative Sectors: All others were lower.

One Month Winners: Materials, Energy, Industrials, Real Estate and Consumer Defensive of note.

Three-Month Winners: Materials, Industrials, Energy, Healthcare and Financials of note.

Six-Month Winners: Materials, Healthcare, Communication Services, Industrials and Energy of note.

Twelve-Month Winners: Materials, Communication Services, Industrials, Technology and Financials of note.

Year to Date Winners: Materials, Industrials, Energy, Consumer Defensive and Real Estate of note.

Bolded means the Sector is new to the period in which it falls.

Upcoming Earnings Of Note: (Erlanger Chartroom Software – sorted by market cap, highest to lowest with most visible names)

Today After the Close: None of note.

Monday Before The Open:

Notable Earnings of Note This Morning:

Beat: PIPR +2.14, AER+0.52, BIIB +0.36, AN +0.19, IMVT +0.10, UAA +0.10, PRLB +0.09, PWP +0.07, MKTX +0.04 and CNC +0.03

Missed: RXO -0.03 of note.

Still to Report: CG CBOE NWL NVT PM PAA ROIV of note.

Company Earnings Guidance:

Positive Guidance: After The Close & This Morning - None of note.

Mixed - None of note.

Negative or Mixed Guidance: After The Close & This Morning - None of note.

Advance/Decline Daily Update:

Gap Ups & Down In Early Pre-Market: (+2% or down more than -2%):

GapUp: QNST +22.8%, EHC +16.5%, BILL +15%, BE +14.8%, NVST +14.4%, PRLB +13.3%, RBLX +13.1%, RDDT +12.4%, DAVE +11.6%, MITK +7.7%, MSTR +7.3%, OTEX +6.6%, ADPT +6%, ATR +4.9%, MRVL +4.5%, SSNC +4%, LUMN +3.9%, RAMP +3.8%, COUR +3.7%, CUZ +3.6%, GEN +3.1%, YMT +3%, POST +2.8%, EQR +2.8%, IREN +2.7%, WMG +2.5%, WRD +2.3%, TM +2.3%, ZS +2.2%, VSAT +2.1%, FTNT +2.1%, G +2.1%, MGY +2.1%, FMNB +2%, TEAM +2%, CDP +2%,of note.

GapDown: DOCS -29.8%, ASYS -29.4%, PI -29.1%, MOH -28.2%, STLA -26%, HUBG -25.1%, RBBN -22.1%, AOSL -15.1%, NWL -11.9%, RXO -10.7%, COTY -10.2%, POWI -8%, AMZN -7.3%, NVT -6%, WERN -4.9%, ILMN -4.9%, PCTY -4%, UNM -2.9%, CNC -2.9%, MTD -2.4%, of note.

Insider Action: None sees Insider Buying with dumb short selling. None sees Insider Buying with smart short sellers. Above $100,000 in purchases with high shorts but no history: GLXY.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

WSJ Lead Story: The Week That Anthropic Tanked The Market and Pu. (WSJ)

Markets Wrap: from Bloomberg

NY Times Business Section Lead Story: Crypto Takes Deep Slide Despite Trump’s Support. (NYT)

Bloomberg Lead: Big Tech To Spend $650 Billion. (Bloomberg)

Thoughtful Money: Stocks Rebound After Tech Rout (Podcast)

Economic & Geopolitical:

Federal Reserve Speakers of note today:

Fed Speakers: None of note.

President Trump’s schedule for today:

Heads to Palm Beach this morning.

Signs Executive Orders at 3:00 p.m. EST.

Economic Data Out -

Weekly

Baker Hughes Rig Count is due out at 1:00 p.m. EST.

Monthly

February University of Michigan Consumer Sentiment is due out at 10:00 a.m. EST and expected to come in at 54.3 from 56.4 in January.

December Consumer Credit is due out at 3:00 p.m. EST and is expected to go to $8.4 billion from $4.2 billion in November.

M&A Activity & Daily Changes: None of note.

Moving Average Table: 40% from 53% of Equities are Positive, and 25% from 8% Bonds are Negative.

Meeting & Conferences of Note:

Sellside Conferences:

DA Davidson Midwestern Bank Summit

BMO Infrastructure & Utilities Conference

Goldman Sachs: Energy Symposium Week

Macquarie China Consumer Channel Check Day

Oppenheimer Emerging Growth Conference

Top Analyst, Investor: None of note.

Shareholder Meetings: None of note.

Fireside Chat: None of note.

FDA Presentation: None of note.

R&D Day: None of note.

Meetings:

Federal Reserve Bank of Chicago Automotive Insights Symposium

Lake Street Life-Sciences Invitationa

Noble Capital Markets Emerging Growth Virtual Equity Conference

Small Cap Growth Investor Conference

Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

Upgrades: ARES EL VST of note.

Downgrades: HUBG of note.